Inventory financing is a type of business credit that helps sellers purchase inventory without paying for it upfront.

On the surface, it sounds like a perfect fix — restock fast, boost sales, and repay later. But many sellers soon find themselves caught in a cycle where things don’t go as smoothly.

Sales don’t always match expectations, inventory remains unsold, and interest or service fees pile up. Before they know it, repayment dates arrive — and without enough revenue, they’re dipping into personal savings just to stay afloat.

That’s why inventory financing requires more than approval—it requires planning, clarity, and the right fit.

In this blog post, we discuss the most common types of inventory financing, the hidden costs that go unnoticed, and how to choose the option that best suits your cash flow and risk tolerance.

What Is Inventory Funding?

Inventory financing allows e-commerce sellers to purchase stock without paying for it upfront. Instead of using their own capital, they secure funding from a lender to buy inventory and repay over time, after selling the products. This allows sellers to expand their inventory without the immediate financial burden.

But the unsold inventory and mounting interest or fees make it difficult to repay on time, leading sellers to dip into personal savings to cover the costs.

That’s why it’s important to understand what makes inventory financing more manageable. Clear, upfront pricing and flexible repayment terms give sellers room to breathe.

With these features, you know exactly how much you’ll repay and when, making it easier to plan for marketing, restocking, or seasonal promotions. Once you understand these trade-offs, you can weigh the risks and choose the financing option that fits your cash flow and sales cycle best.

Types of Inventory Financing

Sellers have multiple options for financing inventory, each with its structure and repayment model.

Some provide lump-sum cash, while others let you borrow as needed or pay suppliers directly. Choosing the right one depends on your cash flow, repayment ability, and sales predictability. Here is a quick breakdown of the most common inventory financing methods:

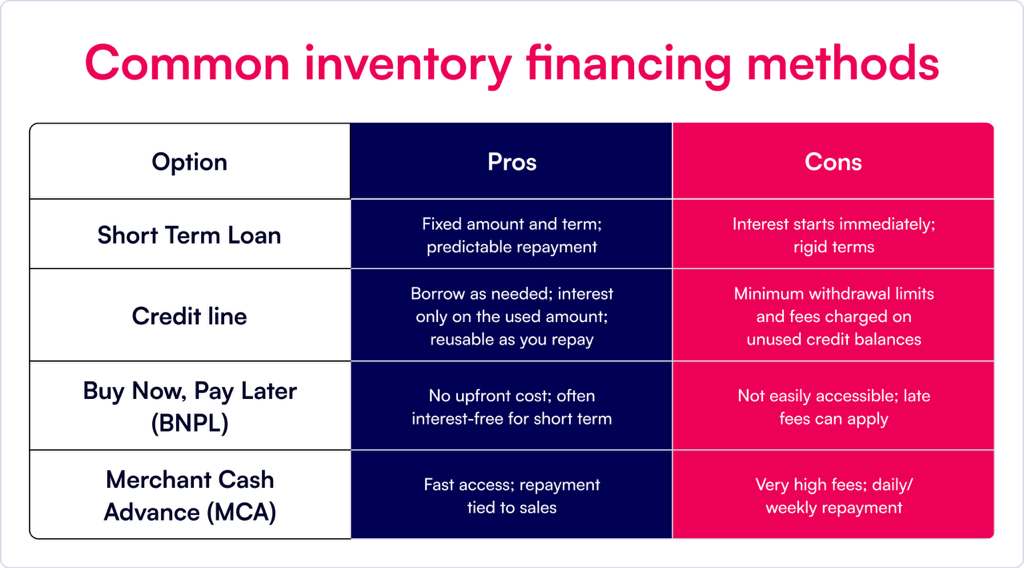

1. Short-Term Loan

This is a one-time loan used to buy inventory. You pay it back over a few months with interest.

Since repayments are fixed, it’s easy to plan for. It’s great if you know exactly how much stock you need and have a good idea of how quickly it’ll sell.

But the interest starts ticking right away, and you’ll need to repay the full amount whether or not your products sell as expected.

2. Revolving Credit Line

A credit line works like a credit card — you’re given a spending limit, and you borrow as needed.

You only pay interest or fees on what you use. It’s helpful if you restock often or need breathing room for unexpected needs.

But it’s easy to keep dipping into it and borrow more than you can repay, especially if your sales are slower than expected.

3. Buy Now, Pay Later (BNPL)

BNPL lets you purchase inventory now and pay for it after a set period, typically 30, 60, or 90 days.

It’s often available only when you buy from approved suppliers or marketplaces, such as Amazon sellers using BigCommerce or Shopify stores partnered with financing platforms like Wayflyer or Uncapped.

If you repay on time, you usually pay no interest, just a fixed service fee, or nothing. But if sales are slower than expected, you may miss the due date and face late fees or blocked access to future BNPL offers.

4. Merchant Cash Advance (MCA)

An MCA gives you an advance based on expected future sales and takes repayment as a daily or weekly percentage of your revenue.

It’s quick and doesn’t come with fixed interest—instead, you agree to a factor rate (e.g., 1.3x the amount borrowed). This method works when you need immediate cash and have consistent daily sales.

But the repayments become burdensome, especially during slow weeks, and the overall cost tends to be much higher than other options.

How to Choose the Right Type of Inventory Financing

Choosing the right type of inventory financing helps manage cash flow without risking your business’s profitability.

Here are the key factors to consider when deciding which option best suits your e-commerce store.

1. Understand your sales cycle

Do you have fast-moving stock with high demand, or slower-selling items?

Tie your credit decision to past sales, demand signals, and pre-orders to make a more accurate forecast of how quickly you can sell the inventory.

The quicker you sell, the more suitable a short-term loan or BNPL is, as these options allow you to repay quickly without tying up too much capital for long periods.

For slower-moving stock, a line of credit or MCA works better since you have more time to sell and repay.

2. Assess profit impact

Will the repayment eat into your profits?

Always calculate the cost of your financing over the repayment period and compare it to your expected sales and profit margins.

You need to ensure that the cost of financing doesn’t outweigh the money you make from sales.

For example, if you borrow $10,000 with a 20% interest rate, you’ll pay back $12,000, but if your profit margin is only 15%, that leaves you with a loss.

3. Align sales timeline with repayment terms

How long does it typically take you to sell off a particular inventory batch? How long will it take to repay the financing?

If you need more time to sell, consider options like revolving credit lines, which allow you to borrow and repay multiple times.

Your repayment cycle should align with your expected sales timeline to avoid late fees and overlapping repayments that strain your cash flow.

4. Have a backup plan in case sales slow down

What happens if your sales don’t meet expectations?

Plan out discount strategies, bundles, or flash sales to ensure you can boost sales if needed.

Having a strategy to sell off slow-moving products reduces the pressure of repaying your financing on time.

5. Review terms and conditions

Before committing to any financing option, understand all the terms and conditions. This includes collateral valuation, creditworthiness assessments, and the repayment terms (fixed or variable).

Some financing options might require you to pledge assets as collateral, so check if you’re comfortable with this.

Read the fine print carefully to avoid hidden fees and conditions that could complicate repayment.

6. Understand the repayment structure

Know exactly how repayment works. Here are some questions to ask:

- Is repayment fixed or based on sales? Fixed repayments feel safer, but strain cash flow, while sales-based repayments are tied to your performance.

- Is there a grace period before repayments start? Some lenders offer a grace period to give you time to sell your inventory before repayments begin.

- Are there penalties or late fees? Late payments lead to extra costs, so know how penalties work.

- What fees are involved? These could include origination fees, processing fees, servicing fees, and others. While some lenders break these out separately, CrediLinq offers a single flat service fee that covers all costs, with no hidden charges.

Inventory Financing Eligibility

When applying for inventory financing, lenders assess key factors to determine whether you qualify. These include your revenue, inventory value, and sales history.

Lenders want to see that your business has steady cash flow, a reliable sales track record, and sufficient inventory to support the financing.

Minimum requirements

Each lender has different criteria, but there are common minimum requirements that most e-commerce sellers need to meet:

- Monthly revenue: Typically, lenders require a minimum monthly revenue, often between $5,000 to $10,000, depending on the lender.

- Account age: Lenders prefer businesses with at least 6 months to 1 year of operational history.

Why some sellers get rejected

Sellers might be rejected for a variety of reasons.

A low sales history, insufficient inventory value, or inconsistent cash flow are common causes.

Lenders may not approve the financing if your business isn’t performing as expected or if you have a higher risk profile. Additionally, poor creditworthiness or failure to meet the required minimum revenue also results in rejection.

Optimizing Inventory Financing

When optimizing your inventory financing, the key is to mix up your sources and start with smaller credit if you’re unsure.

By combining different types of financing, like short-term loans, revolving credit, and BNPL, you create a balanced approach that works for various stages of your sales cycle.

For example, a revolving line of credit is especially useful during seasonal or promotional periods, providing flexible funding to buy fast-moving inventory while allowing you to borrow and repay on your own schedule. This flexibility means you don’t have to tie up all your capital in inventory—you can also invest in marketing campaigns and other growth activities simultaneously.

Meanwhile, BNPL is helpful if your sales are slower and you need more time to pay for inventory. It lets you get what you need now and spread out the payments over a longer time without worrying about paying everything right away.

If you’re uncertain about your sales volume, it’s best to start with smaller amounts of credit.

A short-term loan for just a small batch of inventory lets you test your sales without committing to large sums of money. As sales increase, you can scale your financing to match the demand.

BNPL, Loans, Credit Line—Which One Actually Makes You Money?

Inventory financing isn’t just about choosing a loan, line of credit, or BNPL—it’s about knowing what each one truly costs.

A flat fee makes this simpler because you know upfront exactly how much you’ll pay—no surprises later.

Unlike monthly fees or daily repayments that add up over time, a fixed fee stays the same whether you pay back quickly or take longer. This predictability helps protect your profits and makes planning easier.

Convert every offer into numbers: how much are you borrowing, how much are you repaying, and what’s left after? That’s your real cost.

The best option is the one that matches your sales cycle, gives you enough room to sell, and still leaves you profitable after repayment. Ultimately, pick the financing that works for your cash flow, not just the one that’s easiest to get.

Frequently Asked Questions (FAQs)

1. Is inventory financing risky?

Inventory financing can be risky if sales don’t meet expectations. Interest and fees accumulate while repayment is tied to inventory movement. If stock remains unsold, it leads to cash flow issues and potential debt.

2. Can I get funding without a credit history?

Yes, some lenders like Credilinq offer inventory financing without relying heavily on your credit history. Instead, they focus on your business’s revenue, sales history, and inventory value to determine eligibility.

3. What happens if my inventory doesn’t sell?

If your inventory doesn’t sell, it could lead to additional fees, penalties, or even more debt. Some lenders offer extended repayment terms, but plan for slow sales in advance.

4. How much inventory financing can I qualify for?

Your qualifying amount depends on your sales history, inventory value, and monthly revenue. Typically, lenders offer 50-100% of your inventory value, but it varies based on your business’s financial health.

5. Can I use funding for ads and logistics too?

Generally, no. Most inventory financing options are specifically for purchasing inventory. However, if you’re using a revolving credit line, you can allocate funds for other expenses like ads, marketing, or logistics.