Alternative Lenders: Top 8 Options For e-Commerce Sellers in 2026

TL;DR

- Rising costs in inventory, ads, and shipping, combined with unpredictable cash flow, make flexible financing essential for e-commerce sellers.

- Traditional banks often don’t keep up. With strict requirements, slow approvals, and collateral demands, sellers are left waiting when they need funds the most.

- Alternative lenders bridge this gap by offering capital based on your sales performance.

- From revenue-based financing to resolving credit lines, the alternative lenders make it easier for e-commerce sellers to restock, run ads, and grow without waiting weeks for approvals.

- CrediLinq stands out by offering up to $2M in credit based on real-time sales data, with approvals in as little as one business day and fees as low as 1.5% per month or a simple fixed annual percentage rate (APR) of 18% on the amount used.

Why This Matters to You:

- Cash flow fuels growth.

Even profitable stores struggle when payouts lag, fees add up, or upfront costs eat into your balance. Fast, flexible capital keeps you moving without missing opportunities. - Traditional loans are outdated.

Banks still want collateral, long credit histories, and piles of paperwork—but e-commerce does not work that way. Modern lenders are built for digital-first sellers. - Funding that moves with your sales.

Real-time sales data means fairer offers that scale as your store grows, whether you sell on Amazon, Shopify, or TikTok Shop. - Agility is your edge.

The right financing helps you restock, boost ads, or expand into new markets without waiting weeks for approvals.

For e-commerce businesses, costs hit early before cash comes in for inventory, fulfillment, and ads. That cash gap can stall growth fast.

Banks don’t solve the problem. They ask for collateral, long credit histories, and take weeks to approve.

That is where alternative lenders come in. They move quickly, base decisions on your sales data, and offer repayment terms that fit your revenue cycle. Approvals can come in as little as a day, giving sellers the capital they need to restock, scale, and stay competitive.

The market for alternative lending is projected to hit USD 14.4 billion by 2030, growing at a compound annual growth rate (CAGR) of 25.4%, showing how important these lenders have become.

This article highlights the top 8 alternative lenders for 2026, helping you compare funding, repayment, and eligibility to find the right fit for your e-commerce business.

What Are Alternative Lenders?

Alternative lenders are non-bank financial partners that offer faster and more flexible funding than traditional banks.

Banks are struggling to keep up with how small businesses operate today. Traditional lending depends on outdated credit models, extensive paperwork, and rigid timelines that leave merchants waiting weeks for decisions—and even longer for funds.

Alternative lenders, on the other hand, do not ask for collateral, years of records, or heavy paperwork. Instead, they look at real financial data of your e-commerce business to check eligibility, including:

- sales performance,

- marketplace payouts, or

- transaction history.

Based on this, they offer financing options such as revolving credit lines, revenue-based advances, or short-term business loans.

The best part is speed. Once approved, funds reach your business account in days, or even hours. You can use it flexibly to restock inventory, run ad campaigns, or cover delayed payouts.

Top 8 Alternative Lenders For 2026

Choosing the right funding partner can make the difference between stalling growth and scaling with confidence. We have reviewed 8 leading alternative lenders, and here is a clear comparison of each one, so you can quickly spot the best fit for your growth needs.

Now that we have an overview of how each alternative lender performs, let us get into the detailed explanation of each:

1. CrediLinq

Source: CrediLinq

CrediLinq makes financing simple: just connect your store data, apply in minutes, and get your funding approved in as little as 1 business day.

You can access from US$50K to $2 million in working capital without pledging collateral or giving up equity. The platform uses alternative data, such as sales history, payouts, and revenue patterns, along with your Plaid or bank data to quickly and fairly evaluate eligibility. It integrates directly with platforms like Amazon (approved partner in 16 markets), TikTok Shop, Shopify, eBay, and Lazada to turn your transaction data into usable capital almost instantly.

|

CrediLinq eligibility: You’re eligible for CrediLinq if you:

CrediLinq Geo-availability: CrediLinq is currently available in: United States, United Kingdom, and Singapore CrediLinq approval speed: Approvals in as little as 1 business day Credilinq repayment model: Charges a flat service fee starting from 1.5% per month or a simple fixed annual percentage rate (APR) of 18% on the amount you draw. Choose between 3-6* month tenures available and payback in equal biweekly installments.

*Customized solutions are available upon request. Loan tenors can extend up to 12 months on a case-by-case basis |

Pros:

- Flat service fee starting at 1.5% per month (or a simple fixed APR of 18%), with no hidden add-ons or FX markups

- No equity dilution, no collateral, and no personal guarantees required

- Use the funds flexibly for inventory, ads, payroll, or even global expansion

- Choose 3-6 month repayment terms with no penalties for early payment

Cons:

- Only registered businesses qualify; individuals and sole proprietors are not eligible

- Credit limits depend on sales history, so very new or low-volume sellers may qualify for smaller amount

2. Wayflyer

Source: Wayflyer

Wayflyer delivers funds in as little as 24 hours, does not require personal guarantees, equity, or collateral, and supports financing from as low as $5,000 to as high as $20 million.

Wayflyer offers three distinct funding products, including cash advance, term loan, and rolling finance, each tailored to different stages of e-commerce growth.

- Cash Advance is best suited for new brands, repaid as a percentage of daily sales (revenue-based).

- Term Loan works well for growing businesses, repaid in fixed installments on a set schedule.

- Rolling Finance is aimed at established sellers, with the flexibility to choose between sales-based or fixed repayments, and continued funding access under a 12-month contract.

|

Wayflyer eligibility: A minimum average monthly revenue of $10,000 if incorporated in the United States, Canada, United Kingdom, Australia, Ireland, or Belgium, or $20,000 if incorporated in Spain, the Netherlands, Denmark, Sweden, or Germany. Sellers of physical goods or digital products (e.g., SaaS) need at least 6 months of operational history, while other business types need at least 2 years of trading history. Wayflyer approval speed: Receive funding offers within hours and funds within one business day Wayflyer repayment model: Repayments differ based on the product chosen:

|

Pros:

- Up to $20 million in credit limit, suitable for large inventory purchases or aggressive marketing pushes

- Supports offline sellers as well as online stores, offering flexibility for hybrid businesses

Cons:

- Requires detailed paperwork and verification, which can slow approvals

- Multiple integrations (Shopify, WooCommerce, bank accounts, payment gateways, etc.) needed, which can be time-consuming

- Dropshipping businesses not supported, limiting eligibility for some e-commerce sellers

3. Clearco

Source: Clearco

Clearco provides non-dilutive capital to e-commerce and retail businesses through multiple funding products, each tailored to specific cash-flow needs:

- Invoice Funding: Lets you pay suppliers or manufacturers directly without tying up working capital, while you repay in fixed weekly installments

- Receipt Funding: Reimburses business expenses you’ve already paid helping you free up cash to reinvest in growth

- Cash Advance: Offers a lump-sum capital injection for short-term needs. Repay weekly, with payments capped at 30% of revenue for flexibility during slower sales periods

- Rolling Funding: Provides ongoing access to capital by automatically refreshing your available balance as you make repayments. This gives you a continuous, credit-like experience.

Businesses can typically secure between $25,000 and $600,000 for Cash Advance, depending on their revenue performance, repayment history, and overall business health.

|

Clearco eligibility: Applications remain the same across products, where one qualifies if they are incorporated in the United States and hold a valid U.S. checking bank account. Companies are also required to have at least 12 months of revenue history and generate a minimum monthly revenue of US $10,000. Eligibility and funding capacity are determined by the proprietary Clearco Score, which evaluates multiple factors like:

Clearco Geo-availability: Primarily operates in the United States and serves U.S.-incorporated businesses Clearco approval speed: Approvals are generally processed within 24 hours, with funds released to the business account in about two business days Clearco repayment model: Repayments are structured as fixed weekly installments on a weekly capped payment cadence. Payments continue until the flat financing fee is covered, and early repayment is allowed with pro-rated fee adjustments |

Pros:

- Multiple funding products (Invoice, Cash Advance, Rolling Funding) tailored to varied capital needs

- Predictable, capped weekly payments that scale with revenue, offering protection during low-sales weeks

- Enable early payoff with pro-rated adjustment (you can pay early without penalty), which can help you reduce costs

Cons:

- Limited to U.S.-incorporated businesses with at least 12 months of operating history

- Minimum monthly revenue requirement of $10,000 may exclude newer or smaller sellers

4. SellersFi (formerly SellersFunding)

Source: SellersFi

SellersFi is a financing platform built for e-commerce and Amazon sellers, offering funding solutions that grow with your business. Instead of a one-size-fits-all loan, SellersFi provides four core products to solve different cash flow challenges: Working Capital, CommercePay, Inventory Solutions, and Daily Payout.

- Working Capital: Short-term funding to cover everyday operational needs. Funding from $5,000 to $2.5million, with terms of 3–15 months and approval in as fast as 48 hours

- CommercePay: An advance of your sales, where you repay a set percentage over time (revenue-based financing style)

- Daily Payout: Get up to 90% of your previous day’s Amazon sales, so you are always prepared to purchase for growth

|

SellersFi eligibility: To qualify for SellersFi financing, businesses generally need at least six months of sales history and average monthly sales of $20,000 or more. Eligibility requirements may vary slightly by product but typically apply across Working Capital, CommercePay, and Daily Payout solutions. SellersFi Geo-availability: Serves e-commerce businesses registered in the United States, United Kingdom, Canada (excluding Quebec), and Australia SellersFi approval speed: Approvals can be processed in as fast as 48 hours SellersFi repayment model:

|

Pros:

- High credit capacity up to $10 million for established Amazon sellers

- Interest-only repayment options reduce strain during slow periods

- No personal guarantees required for draws above $250,000

Cons:

- Minimum eligibility (6 months + $20K monthly sales) excludes smaller sellers

- Heavily focused on Amazon and marketplace sellers, less suited for D2C-only businesses

5. OnDeck Capital

Source: OnDeck

OnDeck provides traditional small business financing tailored to entrepreneurs and e-commerce sellers. It offers two main products: term loans and lines of credit.

- Term loans: Borrow between $5,000 and $250,000 with repayment terms of up to 24 months

- Lines of Credit: Access $6,000 to $200,000 as a revolving credit line. Draw only what you need, when you need it, and pay interest on just that amount.

|

OnDeck Capital eligibility: To qualify, businesses must have:

OnDeck Capital Geo-availability: United States, Canada, and Australia

OnDeck Capital approval speed: Applications are submitted online, decisions can arrive in minutes, and approved businesses often receive funds on the same day.

OnDeck Capital repayment model: For term loans, repayments are made through daily or weekly payments over terms of up to 24 months.

For lines of credit, repayments are flexible, with options for 12, 18, or 24-month terms, and can be scheduled as weekly or monthly payments depending on business preference.

Businesses can also reapply for additional funding once repaid 40% of their loan or completed six months of repayment.

|

Pros:

- Access to both term loans and lines of credit gives flexibility in choosing lump-sum vs revolving funding

- Extremely fast approval and same-day funding for many applicants

Cons:

- Reapplication after partial repayment for continued capital access

- Best suited for businesses with stronger credit profiles

- Repayment via daily/weekly deductions means revenue spikes still come with higher repayment obligations in those periods

6. Funding Circle

Source: Funding Circle

Funding Circle provides small business loans and lines of credit for growth-focused SMEs.

- Small Business Loans: Borrow between £10,000 and £750,000 with fixed terms

- FlexiPay Line of Credit: Borrow up to £250,000 with flexible repayment options

|

Funding Circle eligibility: Businesses must have been trading for at least 1 year and must be based in the UK.

Applicants are required to submit up to eight months of recent business bank statements showing account details and daily transactions. Latest full unabridged financial accounts, including a profit and loss statement and a balance sheet is also required.

Funding Circle Geo-availability: United Kingdom

Funding Circle approval speed: Decisions are made within as little as 1 hour, and funds are typically paid out within 48 hours after acceptance

Funding Circle repayment model: For Business Loans, fixed monthly repayments over 6 months to 6 years, with interest rates starting at 6.9% per year and a one-time completion fee at issuance.

For FlexiPay Line of Credit, repay over 1, 3, 6, 9, or 12 months, paying a flat transaction fee starting at 1.99% with 0% interest. Early repayment helps reduce future fees.

|

Pros:

- Provide relatively low interest rates for qualified, established businesses

- Monthly repayment schedule, easier for budgeting

Cons:

- Requires at least two years of trading history and financial statements

- Only available to established businesses, less suited for start-ups or early-stage sellers

- One-off completion fees increase upfront borrowing costs

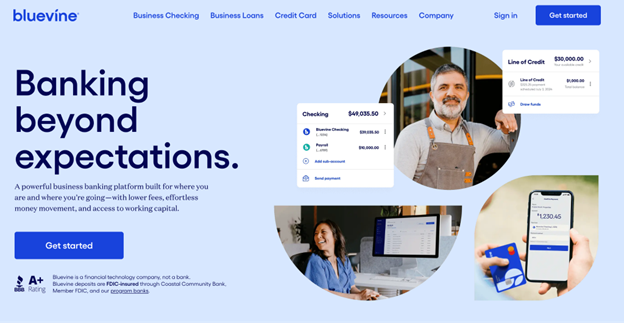

7. Bluevine

Source: Bluevine

Bluevine provides flexible business lines of credit for small business owners to mid-sized e-commerce sellers that need fast, on-demand access to working capital. Businesses can access credit lines up to US $250,000, paying interest only on the amount they use.

|

Bluevine eligibility: To qualify for a Bluevine Line of Credit:

Bluevine geo-availability: Incorporated or operating in an eligible U.S. state

Bluevine approval speed: Credit decisions are typically made within minutes, and qualified borrowers can receive funds within 24 hours Bluevine repayment model: Borrowers can choose repayment schedules of 6 or 12 months, with either weekly or monthly repayments. You only pay interest on what you use, and there are no penalties for prepayment. |

Pros:

- Revolving structure helps e-commerce sellers with irregular sales patterns

- Only pay for what you draw rather than the whole limit

Cons:

- Only available to U.S.-based businesses

- Instant transfers require dedicated Bluevine checking account

8. Fundbox

Source: Fundbox

Fundbox is a small-business financing platform offering revolving lines of credit and short-term working capital solutions. You can borrow up to $250,000 in funding to cover expenses, manage cash flow gaps, or seize growth opportunities.

|

Fundbox eligibility: To qualify, applicants typically need:

Fundbox Geo-availability: Available to businesses registered and operating within the 50 U.S. states, as well as in Guam, American Samoa, the Northern Mariana Islands, Puerto Rico, and the U.S. Virgin Islands. Fundbox approval speed: Provides credit decisions within minutes, though some cases may take up to 24 hours. Approved applicants can receive funds as soon as approved and deposit in their bank account within 2 business days. Fundbox repayment model: Businesses can choose 12-week or 24-week repayment plans depending on their approval terms. Fees start at 4.66% for 12-week plans, varying by applicant. You can repay early anytime, and Fundbox waives all remaining fees. There are no prepayment penalties, and all costs are clearly shown before you draw funds. |

Pros:

- Offers fast funding (often next business day) for qualifying draws

- Only pay fees on the amount drawn rather than entire credit limit

Cons:

- Short repayment terms (12–24 weeks) may not suit long-term financing needs

- Requires connecting bank or accounting software for eligibility

Why CrediLinq Is a Strong Alternative Lender For E-commerce and Retail?

While there are many funding options in the market, few are built exclusively around the realities of online retail. CrediLinq is more than a lender, it is a growth partner for e-commerce brands.

Unlike traditional banks or generic traditional lenders, CrediLinq underwrites based on your real-time sales and marketplace data. That means approvals happen in as little as one business day, and sellers can access up to $2 million without collateral, equity dilution, or personal guarantees.

Here is what makes CrediLinq stand out in 2026:

- E-commerce-first eligibility: If you are selling on Amazon, Shopify, TikTok Shop, eBay, Lazada, or Shopee with at least $1M annual sales and12 months history, you can qualify. No legacy credit scores or collateral standing in your way. The AI-driven model based on alternative e-commerce data even scales your limit up to $2 million as your sales grow, ensuring you always have room to expand.

- Omni-marketplace coverage: Whether you sell on a single marketplace or across multiple platforms and channels, CrediLinq consolidates your sales data into one unified profile. That means your funding limit reflects your total performance—not just one storefront—giving multi-channel sellers a fairer, more accurate credit assessment.

- Transparent pricing: Pay a flat service fee starting at 1.5% per month. There is no origination, no hidden charges, and no penalties for early repayment. You know the cost upfront, making it easy to plan margins.

- Flexible repayment: Choose repayment cycles of 3-6* months to match your cash flow (*extendable up to 12 months on a case-by-case basis).

- Global expansion ready: With active operations in the United States, the United Kingdom, and Singapore, CrediLinq helps you expand beyond borders without the restrictions of traditional trade finance.

Get started now and access growth funding in minutes.

Frequently Asked Questions (FAQs)

What is the easiest financing to get approved for?

Revenue-based financing and short-term credit lines are usually the easiest. They rely on your real-time sales data instead of credit scores or collateral. Platforms like CrediLinq approve funding based on your store’s performance and can provide up to $2M without the heavy paperwork.

What is the new alternative lending?

The new wave of alternative lending uses AI and marketplace integrations to make funding faster and more flexible. Instead of years of financial history, these lenders connect to your Amazon, Shopify, or TikTok Shop account along with your Plaid or bank account to check eligibility. This makes financing quicker, more accessible, and better suited to e-commerce cash flow.

Who is the easiest company to get a loan from?

Lenders like CrediLinq make it simple. They offer fast approvals, require minimal paperwork, and don’t ask for collateral or equity. By connecting directly to your Amazon, Shopify, TikTok Shop, eBay, Lazada, or Shopee account, along with your Plaid or bank account, they can approve funding in as little as one business day.

What lenders give loans with bad credit?

If your credit score isn’t great, lenders that focus on business performance are your best bet. Platforms like CrediLinq look at your sales history and revenue trends, not just your credit score. If your store is performing well, you could still qualify.

Key Takeaways

- Access to the right financing can be the difference between scaling your e-commerce business or stalling during peak demand.

- In 2026, alternative lenders are the go-to choice for sellers who need speed, flexibility, and transparency.

- The best lender is the one that grows with you. Choose wisely, plan how you’ll use the funds, and treat capital as a tool to accelerate growth.

- If you are looking for a partner built specifically for e-commerce and online retail sellers, CrediLinq stands out with fast approvals, transparent pricing, and platform integration