Key Takeaways:

- Lazada sellers can access financing through platform-integrated loans or third-party fintech providers.

- Loans via Seller Center are typically invite-only and limited to Lazada Wallet use.

- Third-party providers on external sites or in the Lazada Services Marketplace offer more flexibility, with funds disbursed to your bank account for broader business use.

- Loan terms, eligibility, and speed of approval vary widely—some options require minimal paperwork and approve within 24–48 hours.

- For sellers looking to grow across multiple platforms or need more control over fund usage, credit lines like CrediLinq offer a flexible alternative.

For thousands of Lazada sellers across Southeast Asia, that “fuel” often means access to fast, flexible capital. Whether it’s gearing up for a big sale event, restocking bestsellers, or investing in better logistics, cash flow can make or break your momentum.

But for many Lazada sellers, getting a traditional loan just doesn’t fit how their business runs. Banks require collateral, years of financial records, or detailed application documents that don’t reflect real-time sales. That process takes too long, and for fast-moving e-commerce sellers, waiting weeks for approval means missing key growth windows, such as 11.11 or a trending product push.

In this blog post, we will examine different funding options for Lazada sellers, focusing especially on Lazada loans

What Are Lazada Seller Loans?

Lazada seller loans are short-term financing options available to eligible sellers through Lazada’s platform.

These loans are not provided directly by Lazada. Instead, Lazada partners with licensed financial institutions and fintech providers to offer financing.

There are two main types of loans:

- Loans accessible directly within Lazada Seller Central, where application, approval, and loan management happen inside the Lazada platform.

- Loans offered by approved third-party fintech providers, where sellers apply and manage loans outside Lazada on the lender’s platform. These providers access Lazada sales data to assess eligibility.

The key difference is that loans through Seller Central are disbursed into the Lazada Wallet and typically must be used within the Lazada ecosystem, while loans from third-party providers are disbursed externally and can be used more freely.

Loans via Lazada Seller Central

Loans offered through Lazada Seller Central are typically invite-only, based on a store’s performance, sales volume, and account history.

- Once invited, sellers can complete the application process within their Lazada Seller Center account. The process is streamlined within the Lazada platform if your store and Lazada Wallet are already verified.

- Loan eligibility is assessed using factors like monthly sales, fulfillment rates, and customer ratings. Most lenders require a valid ID and may ask for additional supporting documents depending on their policies.

- Repayment terms are often short (typically 3–6 months), with rates and fees depending on the partner and region.

Approved loan amounts are disbursed into the seller’s Lazada Wallet. These funds are typically limited to use within Lazada—for example, purchasing inventory, paying for ads, or boosting operations tied to your Lazada store.

Lazada displays the loan status or balance in Seller Center, but the repayment process is external. Repayments are made directly to the lending partner, usually via bank transfer, bill payment centers, or other channels as instructed by the lender.

Loans via Third-Party Fintech Providers

Some Lazada-approved financing partners operate outside of Seller Center, even though they’re integrated with the platform. These fintech providers connect with your Lazada store to access real-time sales data, helping speed up loan decisions and reduce the need for heavy paperwork.

While the specifics vary by lender, here’s a closer look at how CrediLinq, one of the official Lazada lending partner, provides funding to Lazada sellers:

CrediLinq for Lazada Sellers

CrediLinq offers a flexible credit line tailored for e-commerce sellers, including those on Lazada.

Instead of a fixed loan, sellers get access to a pre-approved funding limit and only pay fees when they draw funds.

- Credit limit: Up to $ 2 million, based on store performance and annual revenue (No bank or financial statements required)

- Platform requirement: At least 3 months of sales history on Lazada

- Minimum annual sales: $ 100,000+ (or local equivalent)

- Approval time: Typically within 24–48 hours

- Service fee: 1.5%–3% per month flat, applied only on the amount used. No hidden fees, early repayment penalties.

Funds are disbursed to your bank account, allowing full flexibility in how the capital is used (e.g., inventory, marketing, logistics). This setup provides sellers with more freedom compared to embedded loans, which are locked within the Lazada Wallet, making CrediLinq’s credit line well-suited for cross-platform growth.

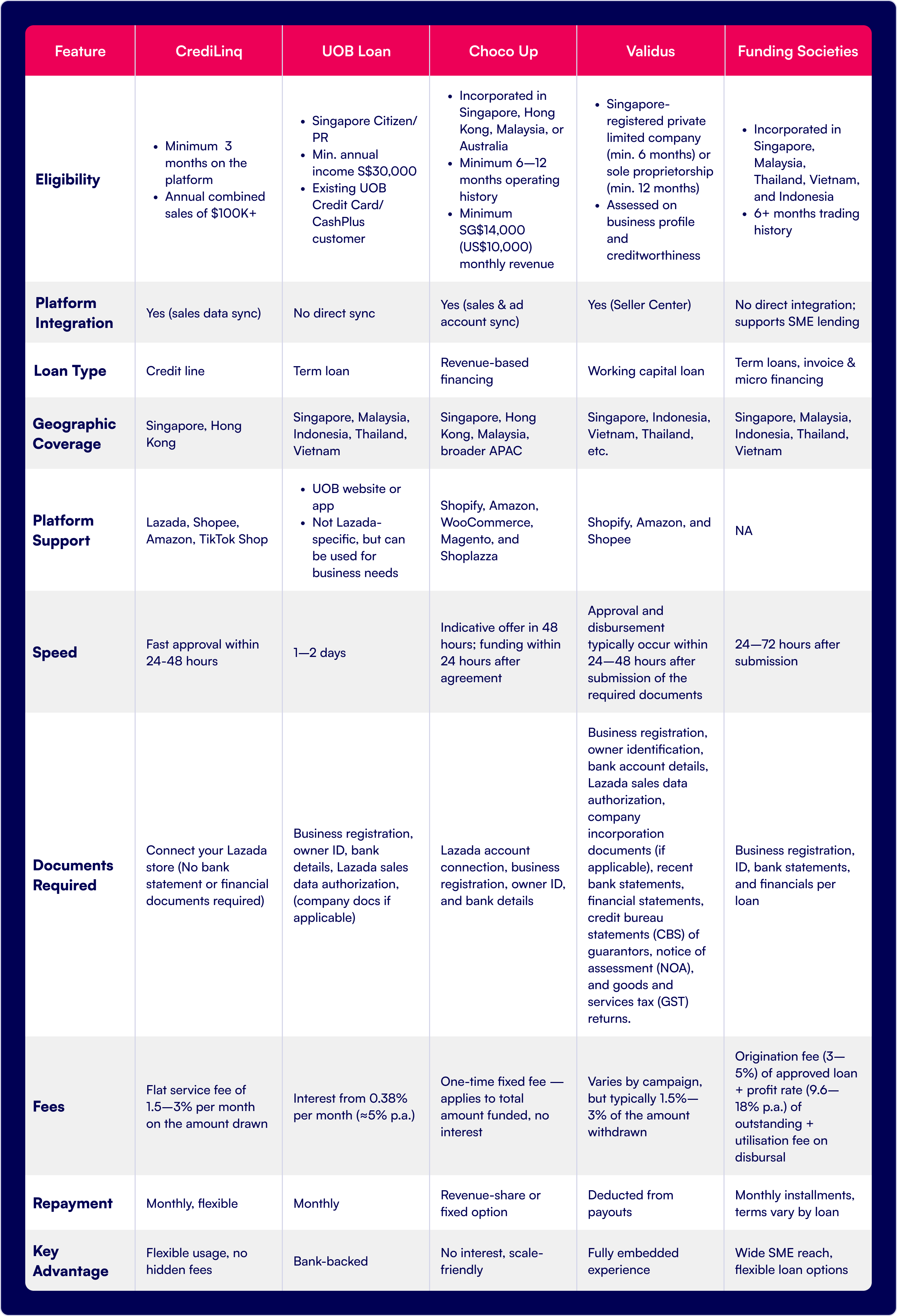

Comparing Financing Options for Lazada Sellers

Lazada sellers have access to a variety of funding solutions, both through the platform and from external fintech providers.

While all of them aim to help sellers manage cash flow and support growth, each provider takes a different approach when it comes to eligibility, loan structure, and repayment terms.

Here’s a quick comparison to help you understand how these options stack up.

Why Consider CrediLinq Over Lazada Seller Loans

While Lazada seller loans can support some sellers by crediting funds to their Lazada Wallet, they are only available to select sellers who meet Lazada’s internal criteria (such as store age and sales performance) and typically range from $5,000 to $500,000, depending on the seller’s eligibility and performance in the Singapore market.

However, CrediLinq is specifically designed for eCommerce businesses that sell on platforms such as Amazon, Shopee, Lazada, and TikTok Shop.

Simply connect your store, and you can access a credit line of up to $2M that grows with your business.

No paperwork, no confusing terms. Just straightforward credit when you need it.

Here’s how it compares:

1. Not based solely on Lazada metrics

Lazada loans are only available to a select group of invited sellers, typically those with established sales volumes on the platform. If your store is new or hasn’t yet reached high sales thresholds, you might not be eligible.

Before you can access a loan, you need to meet Lazada’s internal threshold, which takes time if you’re a new seller or if most of your sales are on other platforms like Shopee, Amazon, or your own website.

On top of this, after meeting Lazada’s internal criteria, you’ll still need to meet the requirements of the dedicated lender offering the loan. This means additional conditions and potentially even more limitations on how much you can borrow.

CrediLinq, on the other hand, considers your complete business health.

Whether you’re generating revenue from Lazada, Shopee, TikTok Shop, or Amazon, your full sales picture is taken into account. This means higher funding potential and fairer evaluations.

2. Use funds freely

Lazada loans are typically geared toward working capital, often with restrictions or expectations about how the funds are used.

CrediLinq gives you the freedom to use the capital where you need it most. Want to run Facebook ads for a product drop? Need to stock up on inventory before a mega campaign? Expanding to new warehouses or third-party logistics partners?

No problem, it’s your call.

3. Clear, transparent terms

CrediLinq makes repayment simple. Terms are transparent, and there are no hidden fees.

With CrediLinq, you’ll know exactly how much you’ll repay and when.

You can choose a repayment period of 30, 60, or 90 days, with a simple service fee of 1.5-3% per month. There are no hidden charges, so you plan your cash flow with full transparency and confidence.

If you’re serious about growing across Lazada, Shopee, and beyond, CrediLinq gives you capital without the platform constraints.

Get fast, flexible funding with CrediLinq.

Frequently asked questions (FAQ)

1. Is Lazada lending available in all countries?

Lazada seller loans are currently offered in select Southeast Asian markets, including the Philippines, Malaysia, Indonesia, Vietnam, and Thailand. However, availability may vary depending on your seller’s performance and whether Lazada has an active lending partner in your country.

2. What if I sell on both Lazada and Shopee — can I still apply elsewhere?

Yes. If you’re a multi-platform seller, you’re not limited to Lazada financing. In fact, platforms like CrediLinq are built for sellers who operate across Lazada, Shopee, Amazon, and TikTok Shop. These solutions offer more flexible, consolidated funding based on your overall sales.

3. How do Lazada loan repayments work?

Lazada loan repayments are usually auto-deducted from your sales payouts in the Seller Center.

For third-party providers, repayments may be made via direct debit or bank transfer, depending on the lender’s terms and whether funds were disbursed outside Lazada Wallet.

4. What are the average loan limits for Lazada sellers?

Lazada loans are primarily based on your sales volume and performance within the Lazada platform. For newer or mid-tier sellers, loan amounts can be quite low. Larger, consistent sellers may qualify for more, but there’s typically a cap based on your Lazada performance alone.

They typically range from S$5,000 to S$500,000, depending on the seller’s eligibility and performance in the Singapore market.

5. What if Lazada rejects my loan? What are my options?

If you’re not eligible for Lazada’s financing or received an offer that’s too small, you still have options. Platforms like CrediLinq let you apply based on your complete sales history, not just Lazada’s metrics.