Highlights

Why This Matters to You

|

There is a concept in statistics called survivorship bias. It is the error of studying only the winners and ignoring the failures. This view can widely distort your understanding of what actually works.

In ecommerce expansion, the same dynamic creates an opportunity, but from the other side. When a market goes through disruption, undercapitalized sellers exit. They liquidate inventory, cut channel investment, or get acquired at distressed valuations.

What they leave behind includes supplier relationships, customer trust in a category, and market share that was being actively contested. The sellers who stayed well-capitalized and kept executing inherit it all. That inheritance is the survivorship bonus.

What is Growth Financing

Growth financing is capital raised specifically to accelerate the expansion of a business. It is different from startup funding, which bridges the gap from zero to initial product-market fit, in that it assumes the business already works.

Growth financing, however, makes sense when you have identified an expansion move such as a new market or channel, a larger inventory position, or a competitor acquisition where the return on deployed capital significantly exceeds the cost of that capital, but the timing gap between deployment and return requires external funding.

Another important distinction to note is that growth financing is not the same as venture capital financing, though the terms are often conflated.

Venture capital is early-stage risk capital betting on an unproven model. Growth financing serves businesses with demonstrated revenue and clear expansion mechanics. The risk profiles are fundamentally different, which is why the costs and structures of each should also differ.

Using VC-style dilutive equity to fund an operational expansion that debt could handle at a fraction of the long-term cost is the most common and most expensive capital structure mistake that scaling eCommerce business owners make.

Table: Differences between startup, VC and growth financing

|

Factor |

Startup Funding |

Venture Capital |

Growth Financing |

|

What it funds |

Getting the business off the ground: product, team, early operations |

Rapid scaling of a proven concept into a large market |

Specific expansion moves: inventory, new markets, acquisitions, working capital |

|

Stage of business |

Pre-revenue or early revenue, unproven model |

Post-product-market fit, high-growth trajectory required |

Established revenue, proven unit economics |

|

What the investor bets on |

The founder and the idea |

The market size and growth rate |

The track record and the deployment plan |

|

Typical structure |

Equity, SAFE, or convertible note |

Equity (Series A, B, C) |

Debt, revolving credit, RBF, or venture debt |

|

Dilution |

High as founders give up significant ownership early |

High as it stacks on top of prior rounds; founders often hold 50% post-Series A |

None to low as debt and revolving credit preserves full ownership |

|

Repayment |

None as investor waits for a liquidity event |

None as investor exits via acquisition or IPO |

Yes, fixed schedule or revenue-linked, depending on structure |

|

Cost of capital |

Highest as early equity is the most expensive capital a founder ever raises |

High as VCs target 25–35% IRR |

Lower as after-tax cost of debt typically 3–8% |

|

Control implications |

Investors often gain board seats or veto rights from the start |

Board representation, protective provisions, exit influence |

Minimal as lenders set covenants; revolving credit typically carries none |

|

Speed to capital |

Slow as due diligence on an unproven business takes time |

Slow because of institutional process, term sheets, legal review |

Fast as marketplace-connected lenders approve in 24–72 hours |

|

Who is it right for |

Pre-revenue founders building something new |

High-growth companies pursuing dominant market positions with a clear exit path |

Established operators fund measurable, time-bound expansion cycles |

The Four Major Growth Financing Vehicles

1. Equity Financing

Equity financing involves selling a percentage of the business to investors in exchange for capital. There is no fixed repayment required, which makes it feel like an advantage. The real cost is invisible at the point of funding and compounds over the life of the business.

These days, equity investors expect 15–25% returns at a minimum. Venture capital funds targeting growth-stage companies look for an Internal Rate of Return (IRR) of about 25–35%.

Also, per Carta’s State of Private Markets, the median seed dilution in 2025 is about 19.5%, and the median Series A dilution is 17.9%. Series A investors typically seek 15–30% ownership. Late-stage valuations remain approximately 40% below 2021 peaks, meaning equity is more expensive in dilution terms today than it was five years ago.

With equity financing, the valuation is more important than the cheque size

Most equity conversations focus on how much is being raised. The number that actually determines how much you give up is the pre-money valuation.

Here is a simple example:

You want to raise $500,000. If your pre-money valuation is $2 million, you give up 20% of the company. If your pre-money valuation is $4 million, you give up 11.1% for the same $500,000. The capital you receive is identical. The ownership surrendered is nearly half.

The median seed pre-money valuation reached $16 million in early 2025, approximately 18% higher than the prior year, meaning founders who pushed on valuation captured meaningfully better outcomes.

The option pool shuffle that blindsides business owners

When investors agree to fund a round, they typically require the company to create or expand an employee option pool. This sounds reasonable. The catch is timing: investors almost always require the option pool to be created before the round closes, which means it is carved from existing shareholders’ ownership rather than from the post-money cap table.

In other words, business owners absorb the dilution from the option pool, not the investors.

Here’s an example:

Suppose you owned 100% of a company valued at $5 million. An investor agrees to invest $1 million but requires that a 15% option pool be created first. That pool carves 15% from the $5 million company. Now, you own 85% before the investor even comes in. Then the investor’s $1 million buys in at the post-pool valuation.

You end up owning considerably less than they expected from a round that was supposed to dilute them by only the investor’s slice. This is called the option pool shuffle, a standard term sheet mechanic that effectively increases dilution by 3–5 additional percentage points beyond what the headline round percentage implies.

Percentage ownership is not the same as what you receive at exit

Owning 40% of a $10 million company is worth $4 million at exit. Owning 20% of a $50 million company is worth $10 million.

A business owner who obsesses over protecting ownership percentage while neglecting drivers of business value, such as margins, repeat purchase rates, channel diversification and supply chain efficiency, often exits with a larger percentage of a smaller outcome. The percentage matters less than the multiple on the underlying value.

An ecommerce seller who uses non-dilutive debt to fund inventory growth, protects margin, and builds a defensible brand, exiting at 4x revenue, will outperform a peer who raised equity at a better headline valuation but sacrificed margin to hit growth metrics for the next round.

|

Best fit for equity financing Equity is rational in a specific set of circumstances, and it is worth being precise about what those are. It makes sense when:

For an established eCommerce seller generating consistent revenue on Amazon, TikTok Shop, or Shopify, using capital for a new channel or market expansion, these conditions rarely apply. The revenue is predictable, the use case for capital is operational, and the investor’s ecommerce-specific expertise is often limited. |

|

Also read: Debt vs. Equity Financing |

2. Venture Debt

Venture debt is a debt instrument designed for high-growth companies, typically structured as a term loan with attached warrants that give the lender a small equity stake. It is cheaper than equity but carries more complexity than a standard credit facility.

The US venture debt market reached $53.3 billion in 2024, nearly doubling from the prior year, as companies sought alternatives to dilutive equity amid a correction. Venture debt typically carries interest rates of 8–15% plus, often accompanied by warrant coverage that provides lenders with additional equity upside.

Demystifying the ignored parts of Venture Debt as a growth financing option

Warrants can come with a high long-term cost

A warrant gives the venture debt lender the right to purchase a percentage of your company’s equity at a fixed price set today. If the business grows significantly in value, the lender participates in that upside in addition to collecting interest on the loan.

Warrant coverage is typically expressed as 10–20% of the loan amount. In terms of equity dilution, that usually translates to 0.5–2% of the company’s total equity, depending on the current valuation.

Here’s an example:

You raise $5 million in venture debt with 10% warrant coverage all on standard market terms. The lender receives warrants to purchase $500,000 worth of equity at today’s price.

If the company’s current valuation is $25 million, then $500,000 represents a 2% stake. If the business exits at $100 million, those warrants are worth $2 million. Effectively making this a 4x return on top of the interest the lender has already collected, on what was effectively a free option embedded in the loan terms.

The warrant conversation also shifted significantly after the collapse of SVB in 2023, which had previously been the largest provider of venture debt to startups.

Surviving lenders became more risk-averse, and several deals have seen warrant coverage in the double digits as a percentage of the loan amount, well above the historical norm, as lenders demand higher upside compensation for the same capital.

Negotiating warrant coverage below 5% of the loan amount should be considered a solid outcome, not even a starting expectation

Venture debt almost always comes with covenants

Lenders often include conditions that restrict what the business can do with the capital or impose financial ratio requirements. These typically include a minimum cash balance the company must maintain at all times, a minimum quarterly revenue target, and a maximum debt-to-equity ratio. This can create operational friction for fast-moving businesses.

The MAC clause is another upside for the lender

Most venture debt agreements include a Material Adverse Change (MAC) clause. This provision allows the lender to call the loan if they determine that the business has materially worsened since the loan was made.

The definition of “material adverse change” is deliberately broad, which gives the lender significant discretion.

In practice, MAC clauses are rarely exercised outside of genuine business deterioration. But for a fast-moving ecommerce business that constantly navigates market changes, the clause can create lender anxiety that triggers uncomfortable check-ins, covenant re-negotiation requests, or pressure to raise equity sooner than planned.

|

Best fit for venture debt Venture debt works best for businesses that already have equity investors in place, since venture debt lenders typically use equity investors as a quality signal in underwriting. It is most commonly used to:

|

3. Revenue-Based Financing (RBF)

Revenue-based financing provides capital upfront in exchange for a fixed percentage of future revenue until a predetermined repayment cap is reached. No equity changes hands. No fixed monthly payment runs regardless of sales performance. At early revenue stages, this flexibility is genuine.

Pros and cons of Revenue-Based Financing (RBF)

Paying it off early does not save you money, and that is by design

With a traditional loan, paying early reduces the total interest paid. Pay off a 12-month loan in 6 months, and you save roughly half the interest.

With RBF, the flat fee is fixed regardless of how long repayment takes. If you advance $100,000 at a 10% flat fee, you owe $110,000, whether you pay it back in 2 months or 8 months. There is no incentive to clear it faster, and no financial benefit if you do.

This also means that paying it back faster actually results in a higher annualized cost, not a lower one.

Clearing a 10% flat fee over 6 months produces an effective APR of approximately 40%. Clearing the same flat fee over 3 months also produces roughly 80% APR. Clearing it in 2 months during a high-revenue period pushes the APR toward 120%.

|

Effective APR = (Flat Fee ÷ Average Outstanding Balance) × (12 ÷ Repayment Months) The average outstanding balance is approximately half the advance amount. This is because the balance declines progressively from the full amount to zero, making the average midpoint roughly 50% of the original advance. Scenario 1: 6-month repayment:

Scenario 2: 3-month repayment:

Scenario 3: 2-month repayment (high-revenue period):

The cost of capital goes up when your business performs well. This structural inversion makes RBF a poor fit for scaling eCommerce business. |

Margin to repayment cadence on RBF can be exhaustive

Most sellers rarely evaluate RBF by comparing the remittance rate to the gross margin.

For example:

If your gross margin is 25% and the provider’s remittance rate is 15% of gross revenue, you would find that you are dedicating 60% of every dollar of gross profit to loan repayment.

That leaves 40% of your margin, before operating expenses to run the business. On a product selling at $100 with a $25 gross margin, every $100 sale sends $15 to the RBF provider and leaves $10 of margin for the business.

As Hahnbeck notes directly in their breakdown on RBF for eCommerce:

“With thin margins, dedicating a significant percentage of your revenue to RBF payments can put a strain on cash flow, limiting operational flexibility.”

Before signing any RBF agreement, divide the remittance rate by your gross margin percentage. If the result exceeds 50%, the facility is consuming the majority of your margin, and the risk is structural.

|

Best fit for RBF RBF works best for one-off capital needs with a defined short cycle in early revenue stages, where the product’s speed and accessibility outweigh its cost. It can work for:

|

4. Hybrid Instruments

Hybrid structures combine debt and equity features, the most common being convertible notes and SAFE (Simple Agreement for Future Equity) agreements. Both defer the pricing of equity to a future round while providing capital now.

A convertible note is a debt instrument that converts to equity at a discount at the next qualifying fundraise. A SAFE is a warrant-like instrument that converts without the debt mechanics.

The maturity date trap in convertible notes

SAFEs have no maturity date. They sit on the cap table indefinitely until a conversion event. Convertible notes do have a maturity date, typically 12–24 months, and this creates a specific risk that most founders underestimate when they sign.

If the company has not raised a priced equity round by the maturity date, the note becomes due for cash repayment, which most early-stage businesses cannot do. This gives the noteholder leverage to negotiate conversion terms at the last minute, often from a position of strength.

A business owner who raised a $300,000 convertible note expecting to close a Series A in 18 months, and who is approaching the maturity date without a round closed, is now in a negotiation where the investor can push for a lower conversion cap or a higher discount in exchange for extending the maturity.

The note that looked founder-friendly at signing looks very different at the 23-month mark with no round in sight.

Practical rule: When using a convertible note, set the maturity date well beyond your planned fundraising timeline, and model what happens if the round does not close on schedule.

|

Best fit for hybrid instruments Great for:

Convertible notes and SAFEs were built for a specific problem: a business too early to value accurately needs capital before it can price a proper equity round. That problem disappears once a business has consistent revenue, established margins, and a track record. This makes it less suitable as a growth financing option for an already established business. |

Real-World Growth Financing Case Study – Razor Group Under Purview

Razor Group, the Berlin-based Amazon brand aggregator, has executed one of the most documented consolidation runs in ecommerce M&A.

On March 5, 2024, it acquired Perch, the leading US Amazon aggregator, in an all-stock deal and simultaneously announced a $100 million Series D round led by Presight Capital, valuing the combined entity at approximately $1.7 billion

Then, in March 2025, Razor itself hit a liquidity wall. The company required $30 million in bridge financing from lenders, including BlackRock and Victory Park Capital Advisors, to remain operational.

A BlackRock middle-market private credit fund holding Razor debt was downgraded. The company that had absorbed four aggregators in two years was now drawing emergency capital to stabilize.

By August 28, 2025, five months after the liquidity crunch, Razor had addressed its bridge financing needs and announced a strategic merger with Infinite Commerce, a $350 million annual revenue business formed by combining four major aggregators.

This was not a distress acquisition. Razor CEO Max Biller leads the combined entity with a stated target of industry-leading profitability in H2 2025 and new growth through M&A in 2026.

Razor Group raises two points worth sitting with:

- First, growth financing deployed into proven assets at distressed prices is a genuinely powerful consolidation strategy; the Perch acquisition demonstrates that clearly.

- Second, the March 2025 liquidity crunch illustrates what happens when a capital stack grows faster than the revenue base supporting it.

Razor raised more than $1.3 billion in total capital. When revenue growth did not keep pace with the obligations created by capital, the company needed emergency financing before it could execute its next strategic move.

The survivorship bonus is real. But the capital structure used to pursue it determines whether the strategy compounds or requires rescue before it can continue.

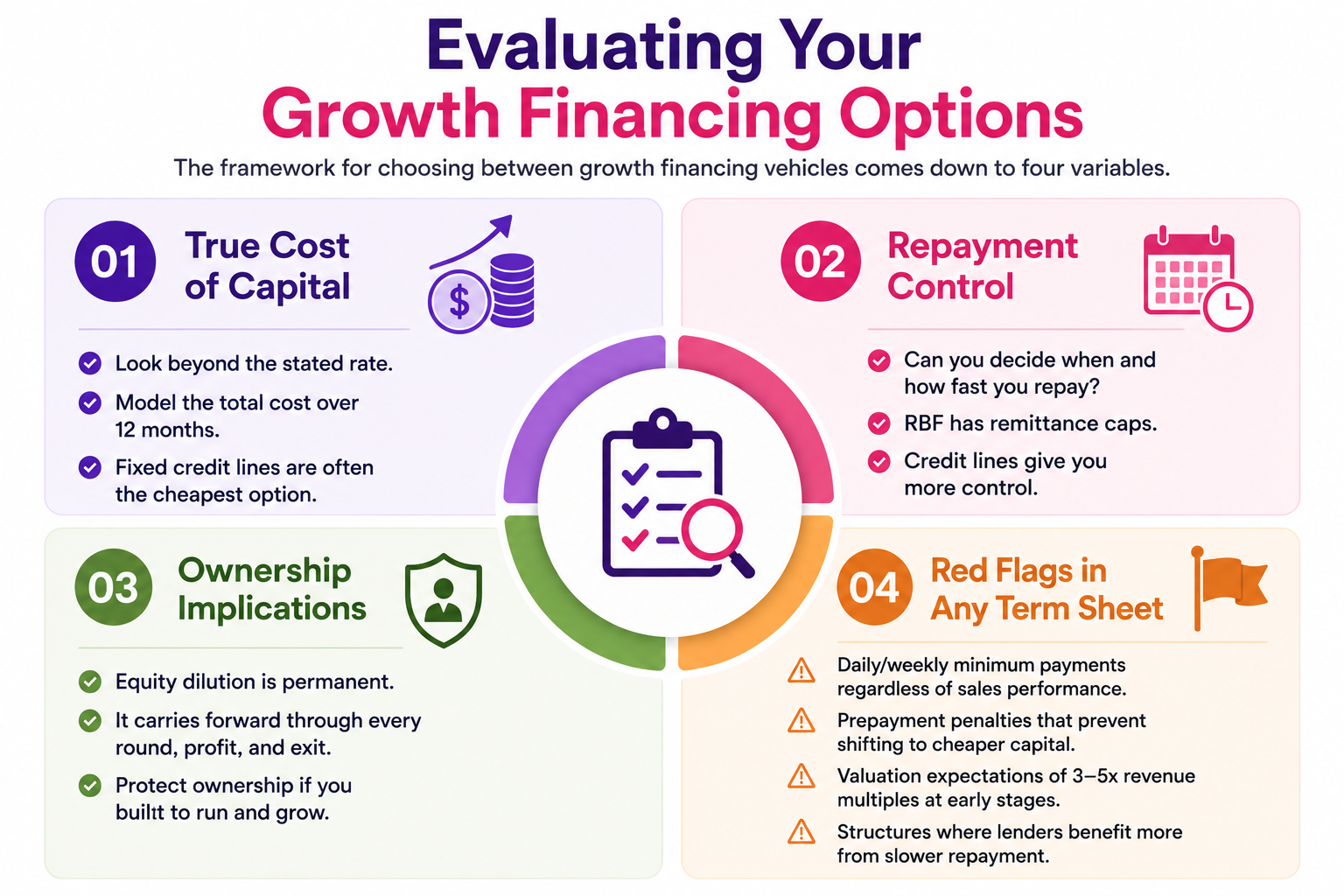

Evaluating Your Growth Financing Options

The framework for choosing between growth financing vehicles comes down to four variables.

Framework for choosing the best growth financing option for you

1. True cost of capital

The stated rate is rarely the real rate. Equity’s cost is invisible. It is found in cap table dilution and future profit sharing. RBF’s cost is understated as the flat fee and remittance rate can inflate the effective APR cost on a standard repayment cycle.

A revolving line of credit at 18% fixed APR is often the cheapest option in annualized terms for a seller with stable revenue doing recurring draws. Model the total cost of each option over a 12-month horizon before selecting.

2. Repayment control

Can you determine when and how fast you repay?

Equity has no repayment requirement, which feels like control but removes the ability to close out the investor relationship. RBF has remittance caps that prevent faster repayment even when cash is available. A revolving credit line is repaid on a fixed schedule controlled by the seller, with the next cycle resetting.

3. Ownership implications

Every percentage of equity sold early is permanent. Equity does not expire at the end of the loan term. It carries forward through every future financing round, every profit distribution, and every exit. For eCommerce owners who built their businesses to run and grow them, not to hand them to investors, this permanence is the most important cost dimension.

4. Red flags in any term sheet

Watch for daily or weekly minimum payment requirements regardless of sales performance, prepayment penalties that prevent shifting to cheaper capital when available, and valuation expectations that require 3–5x revenue multiples at early stages. Any structure in which the lender or investor benefits more from slower repayment than from faster repayment is misaligned with the seller’s interests.

How CrediLinq Supports the Survivorship Bonus Strategy

The survivorship bonus accrues to sellers who can keep deploying capital at every moment when the market creates an opportunity.

CrediLinq provides a revolving line of credit specifically designed for high-growth ecommerce sellers. Underwriting is based on marketplace sales performance across Amazon, TikTok Shop, Shopify, eBay, Lazada, and Shopee, as well as bank statements or Plaid account data.

No physical collateral is required, and you don’t give up any equity. Eligibility requires 12 months of operating history and $30,000 or more in monthly revenue. Draw amounts range from $25,000 to $2M for qualified sellers.

The monthly service fee starts at 1.5% on drawn funds only, with no hidden fees on undrawn balance. Biweekly repayments are done over 3 to 6 months with no early repayment penalty

For growth financing purposes, the revolving structure is important. A term loan or an RBF advance provides a single disbursement with a single repayment schedule.

A revolving credit line is drawn when needed, repaid from the proceeds of that capital cycle, and resets, allowing a seller to fund a bulk purchase order in Q1, repay from Q2 settlements, and draw again for peak-season inventory in Q3 without paying a new flat fee each time.

That recycling of capital across multiple expansion cycles within a single facility is what makes it structurally suited to the recurring growth capital needs of an ecommerce business operating at this scale.

For sellers evaluating the survivorship bonus strategy, using capital to keep executing while the market consolidates around them, the financing structure needs to move at the speed of market opportunity.

Traditional bank financing takes weeks and requires collateral. Equity raises take months and cost ownership. A platform-connected revolving line of credit like CrediLinq’s can be approved in way less time and drawn the same week a supplier window opens, a new channel requires inventory, or a competitor’s retreat creates a category gap.

Choosing Your Growth Finance Strategy

Work through these questions in order before committing to any financing structure.

1. Is the expansion move defined and the return quantifiable?

Growth financing tied to a specific deployment plan, inventory for a new market or funds for a supplier deposit, produces a better risk-adjusted outcome than capital raised against a general growth narrative. Define the use before the amount.

2. Does the business have a stable enough cash flow to service fixed repayments?

If yes, debt is almost always cheaper than equity. If no, and if the expansion itself is what generates the cash flow, then the structure needs to reflect that uncertainty, which may point toward equity or a hybrid.

3. How much ownership are you willing to permanently transfer to solve this problem?

Model the implied exit value of the equity you would sell at current valuation versus the total interest cost of debt over the same period. The gap is almost always larger than founders expect before doing the calculation.

4. Is the capital need recurring or one-time?

Recurring capital needs favor revolving structures. One-time capital needs, like an acquisition or a market entry that requires upfront legal and compliance costs, may favor a term loan or a single advance.

5. What is the 12-month total cost of each option?

Not the headline rate. The annualized cost, inclusive of fees, warrants, dilution, and opportunity cost of ownership surrendered.

Expansion does not wait for perfect conditions. The market consolidations, supplier windows, and category gaps that create the best growth opportunities are time-bound. The sellers who capture them have to be prepared.

Working through these five questions before the opportunity appears is what preparation looks like.

Most founders who work through them discover two things:

- The capital need is more specific than it feels

- The cost of equity is higher than they assumed.

That combination, a defined use case and a clear cost comparison, is what separates a growth financing decision from a general capital raise.

For eCommerce businesses whose needs are operational and recurring, that analysis almost always lands on non-dilutive debt. CrediLinq offers funding types for this exact scenario. You do not give up any equity and can draw on approved amounts at any time you find an ample opportunity.

Final Takeaways

|

Frequently Asked Questions

What is the difference between growth financing and a working capital loan?

Working capital loans cover operational gaps like payroll, inventory shortfalls and cash flow timing. Growth financing funds deliberate expansion moves with a measurable return. The distinction matters because the vehicle, cost, and repayment structure appropriate for each are different.

How do I know if my eCommerce business is ready for growth financing?

Two signals indicate readiness:

- Consistent high-flow monthly revenue with a defined expansion move

- A quantifiable return and a capital gap between when the investment is needed and when the revenue it generates arrives.

If this is the case, growth financing is appropriate. If the business model is still being validated or unit economics are not yet understood, the business is too early for growth financing.

What are the biggest mistakes eCommerce operators make with growth financing?

- First, choosing equity for operational needs — selling ownership to fund inventory cycles that debt could not handle at a fraction of the long-term cost.

- Second, using revenue-based financing as a recurring capital structure, as its effective APR can compound across multiple draw cycles in ways that steadily erode margin.

- Third, accessing growth capital reactively, after the window has already opened, rather than structuring the facility before the opportunity requires it.

References

- https://windsordrake.com/ecommerce-ma-usa/

- https://www.capstonepartners.com/insights/article-e-commerce-sector-update/

- https://www.phoenixstrategy.group/blog/debt-vs-equity-cost-of-capital-comparison

- https://carta.com/data/state-of-private-markets-q1-2025/

- https://www.wsj.com/articles/venture-debt-firms-tilt-toward-mature-companies-98cd30dc

- https://www.hsbcinnovationbanking.com/gb/en/resources/venture-debt-dos-and-donts

- https://www.hahnbeck.com/revenue-based-financing

- https://www.prnewswire.com/news-releases/razor-group-acquires-us-amazon-aggregator-perch-and-announces-series-d-financing-round-302080402.html

- https://www.cbinsights.com/company/infinite-commerce

- https://www.prnewswire.com/news-releases/razor-group-and-infinite-commerce-merge-to-form-the-leading-consolidator-in-the-fba-aggregator-space-302540500.html