TL;DR

- Fast-scaling e-commerce businesses face working capital crunches due to the need for upfront supplier payments, while customer payments are delayed.

- PO financing helps cover supplier costs, allowing you to fulfill large orders without cash flow strain. The lender pays your supplier, your customer repays the lender, and you receive the balance after fees.

- While PO financing avoids equity dilution, the funds are restricted to inventory purchases and not for other purposes, such as marketing or logistics.

- CrediLinq offers flexible credit lines, transparent single-fee pricing, and funding for various business needs like geographical expansion, product launches, marketplace expansion, marketing and inventory, all without requiring collateral or equity dilution. The application process is quick and easy with minimal documentation, and fast approval in as little as 1 business day.

Imagine a skincare brand receiving a bulk order for 5,000 units of its new serum before launch. The product has not been manufactured yet, and the supplier demands full payment before starting production. The brand wants the sale but does not have the cash to cover such a large upfront cost.

This is where purchase order (PO) financing comes in. PO financing allows sellers to accept large B2B orders without holding inventory or upfront cash. With a signed purchase order in hand, sellers can access funding to pay suppliers and fulfill the order, without straining their cash flow.

Why Cash Flow is a Challenge for Growing E-commerce Businesses

Even with strong sales, many e-commerce businesses struggle to keep enough cash on hand to fulfill large orders, restock inventory, or scale operations. Growth outpaces available capital quickly.

Here is why cash flow remains a challenge for growing e-commerce businesses:

Upfront supplier payments vs delayed customer payments

Suppliers typically require payment before shipping goods, while customers may take weeks to pay after receiving their orders. This delay strains working capital, especially for small to medium-sized enterprises (SMEs).

For instance, a 2023 study by Xero revealed that small businesses in the UK experienced an average delay of 6.1 days beyond agreed-upon payment terms, resulting in a cumulative cost of £1.6 billion due to late payments.

Seasonal spikes and bulk order opportunities

During peak seasons, like Black Friday, the holiday shopping rush, or Mother’s Day, sales surge, creating opportunities for bulk orders. However, fulfilling these orders requires substantial upfront investment in inventory and production.

For instance, a small U.S. manufacturing company received a $200,000 purchase order from a major retailer, but faced a challenge. The supplier required $120,000 upfront. With no available cash, the deal was put on hold. By securing PO financing, the manufacturer paid the supplier immediately, produced the goods, and fulfilled the retail order on schedule. Once the retailer paid, the financing company deducted its fee and sent the remaining profit to the manufacturer.

Rapid growth and working capital gaps

When a business scales quickly, costs surge, which means ordering more stock, hiring more staff, and allocating larger marketing budgets to maintain momentum. Even with customers paying on time, these upfront costs often outpace available cash flow, creating short-term working capital gaps that threaten to stall growth.

A 2023 survey by McGrathNicol Advisory found that 73% of CFOs reported having to work hard just to manage working capital, and 70% expected that challenge to grow in the next 12 months.

To manage this cash crunch, many businesses turn to purchase order (PO) financing. It offers a way to secure funds upfront and meet growing demand, without waiting on customer payments.

What is Purchase Order (PO) Financing?

Purchase order financing is a short-term funding method where a third-party lender covers the cost of producing and delivering goods tied to a confirmed customer order. Instead of giving the funds to the seller, the lender pays the supplier directly. Once the end customer pays for the order, the lender collects its share and passes the rest to the seller.

This setup helps B2B sellers take on large customer orders without needing to front the money themselves. Since many buyers do not pay upfront, PO financing reduces the risk of overextending cash reserves and allows sellers to fulfill big orders without straining cash flow.

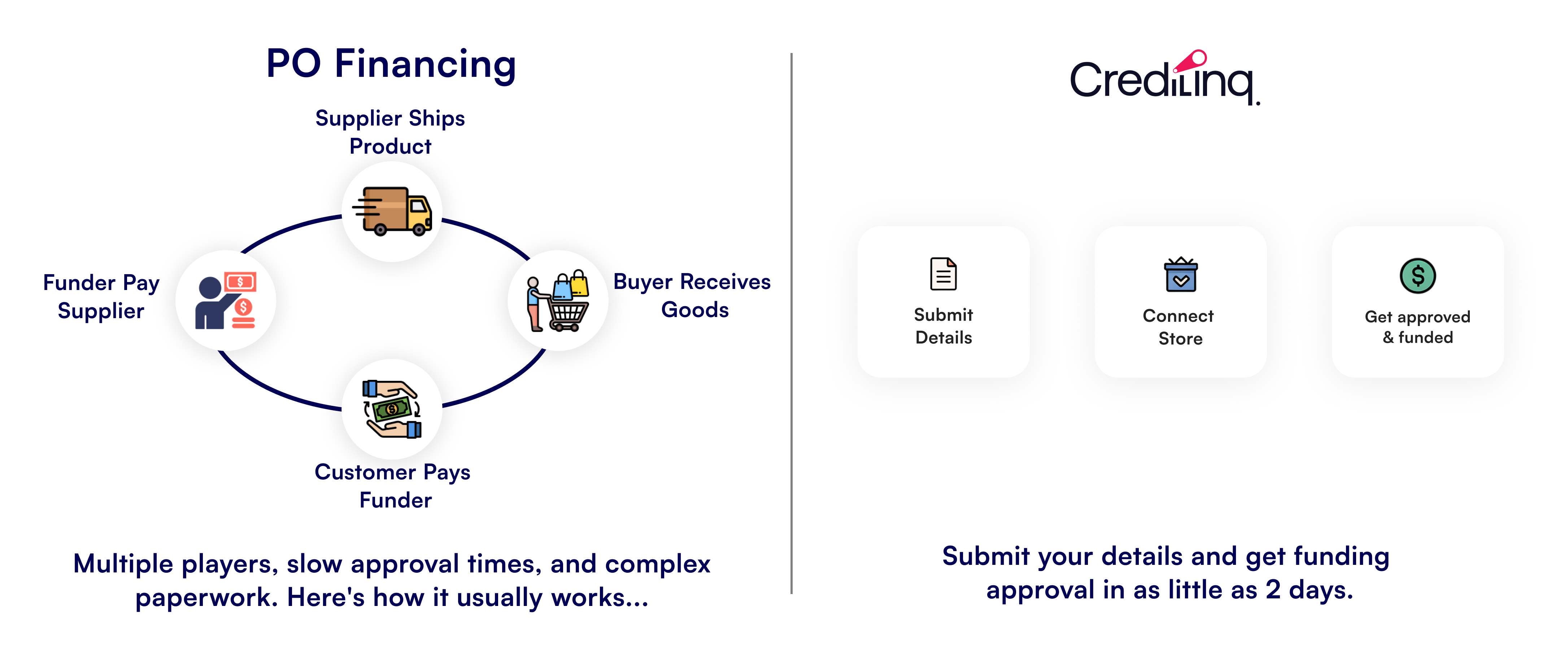

How PO Financing Works?

PO financing works differently from a typical loan. Instead of giving you cash to spend how you want, the financing company pays your supplier directly so you can fulfill large customer orders.

Here is how the whole process plays out:

- PO financing application: Apply to a PO financing company, along with copies of the purchase orders and supplier cost estimates. Lenders often cover up to 100% of the supplier costs, depending on your track record and the reliability of the supplier. If they cover less than the full amount, you will need to make up the rest.

- Supplier payment: Once approved, the lender pays the supplier directly, either in cash or via a letter of credit. Letters of credit are common in international trade and typically require proof that goods have been shipped before the supplier gets paid

- Goods delivery: The supplier produces and ships the goods to your customer as agreed. After delivery, the PO financing company receives confirmation that the order has been fulfilled

- Customer invoicing: Once the customer receives the order, you send them the invoice. Instead of paying you, the customer sends their payment directly to the PO financing company

- Profit receipt: The financing company deducts its fee from the customer payment and sends you the rest. That final amount is your profit from the order, minus the cost of financing.

Pros and Cons of PO Financing for E-commerce Sellers

PO financing offers real advantages for e-commerce sellers, especially when managing cash flow to fulfill larger orders. However, understanding both the benefits and limitations helps you decide if it fits your business needs.

Pros

Access growth capital without equity dilution

PO financing provides much-needed working capital tied specifically to confirmed purchase orders, enabling businesses to take on large or bulk orders without having to give up any ownership or control.

Bridges cash flow gaps in long procurement cycles

Many industries face long procurement and production lead times, especially when dealing with overseas suppliers or complex manufacturing processes. This delay between placing orders and receiving payment from customers creates a cash flow gap.

PO financing fills this gap by advancing funds specifically to cover supplier costs upfront, allowing companies to keep production moving smoothly without waiting for customer payments.

Reduces supplier negotiation friction and strengthens relationships

Since PO financing companies pay suppliers directly and on time, businesses gain stronger credibility and trust with their suppliers. This timely payment often leads to better negotiation power, including extended payment terms, early payment discounts, or priority access to high-demand or limited inventory.

Leverages the creditworthiness of end buyers to unlock capital

Unlike traditional financing options that depend heavily on the borrowing company’s creditworthiness, PO financing assesses the credit profile of the end customer issuing the purchase order, often large, reputable retailers or corporations.

This allows startups and businesses with limited credit histories to access substantial funding by leveraging the financial strength of their buyers.

De-risks the fulfillment of large, seasonal, or one-time orders

Large purchase orders, especially seasonal spikes or unique government contracts, can pose significant financial risk due to the upfront investment required in materials and production. PO financing mitigates this risk by providing funds earmarked explicitly for these orders, thereby reducing the likelihood that cash flow constraints will hinder successful fulfillment.

This enables businesses to confidently accept bigger or one-off deals that can significantly boost revenue and market presence.

Cons

Limited to order-related costs

PO financing is designed strictly for fulfilling confirmed purchase orders. The funds are allocated directly to suppliers and cannot be used for related costs, such as packaging, logistics, or marketing, even if these are essential to the successful delivery of the order.

CrediLinq, on the other hand, offers flexible credit lines that support not only supplier payments but also adjacent business needs, such as restocking, shipping, marketing campaigns, or platform fees through e-commerce financing. This makes it a more scalable option when your growth extends beyond a single PO.

Does not cover the full PO cost

While many PO financing providers cover up to 100% of supplier costs, they typically require strong profit margins, often 25% or higher, for approval. If your business operates on tighter margins, you may struggle to qualify or secure full funding.

In contrast, inventory financing companies may offer greater flexibility, funding stock purchases regardless of customer POs. And with CrediLinq, you are evaluated based on business performance and growth, not just markup, making capital more accessible as you scale.

Scalability and order size limitations

While PO financing can support growing order volumes, the amounts are typically tied to the size of individual purchase orders and supplier terms. This means that firms relying on many small or irregular orders may face challenges in securing sufficient capital.

Additionally, some providers impose limits on maximum funding per order, which can restrict growth during peak seasons or significant expansion efforts.

Operational complexity and additional costs

PO financing involves multiple parties:

- You (the seller/borrower)

- Your supplier

- The PO financing company (lender)

- Your customer (the buyer)

Coordinating payments, deliveries, and invoices adds operational steps that can slow down fulfillment and increase administrative workload.

In addition to the monthly service fee, typically 1–6% of the financed costs per 30 days, lenders often charge extra fees, including:

- Extended-term fees, applied when customer payment extends past the agreed terms

- Wire/transfer charges, for payment handling

- Underwriting or due diligence fees, for validating orders and supplier/customer reliability

- Late-extension or overage fees, charged when repayment delays go beyond the extended period already approved, often after grace terms expire

These combined costs can be significantly higher than those of traditional loans, adding a notable expense that businesses must factor into their budgeting and cash flow management.

Key Benefits of Using a Line of Credit for Purchase Orders for E-commerce Over PO Financing

For sellers who find PO financing too restrictive, a line of credit, such as CrediLinq, offers greater flexibility and cost efficiency in managing purchase orders and inventory in e-commerce.

Comparing Funding Options for Purchase Orders

*Loan tenors can be extended up to 12 months on a case-by-case basis.

Benefits of Using CrediLinq for Purchase Order Funding

While PO financing can be a great option for many e-commerce businesses, CrediLinq brings unique advantages that not only address the everyday challenges of traditional PO financing but also provide added flexibility for e-commerce sellers.

- Use funds across multiple business needs: CrediLinq offers flexible credit lines that can be used not just for supplier payments, but for market/marketplace expansion, new launches, marketing, inventory management, payroll, and other operational needs.

- Full PO cost coverage: Traditional PO financing often requires profit margins of 25% or higher to cover the full order amount. CrediLinq can finance up to 100% of your purchase order cost (up to $2M) based solely on your sales data, helping to reduce cash flow gaps and ease strain during larger or seasonal orders.

- Simplified eligibility requirements: The application process is quick and accessible, requiring sellers to be active on their e-commerce platform for at least twelve months and have at least US$ 1 Million in combined annual sales. By leveraging data from major platforms like Amazon, TikTok Shop, Shopify, eBay, Lazada, Shopee, and other marketplaces, CrediLinq speeds up approval and makes funding accessible even to newer or smaller sellers. This makes it flexible enough to finance multiple smaller orders.

- Scalable financing solutions: With credit lines up to $2 million, CrediLinq enables e-commerce sellers to scale rapidly. There are no order size limits or restrictive caps, meaning you can secure large orders effortlessly. Plus, with global payment support, you can confidently manage international expansions without being constrained by platform-specific limitations.

- Flexible, transparent, and fast funding: CrediLinq provides fast, collateral-free, and equity-free funding with a transparent pricing model (flat service fee as low as 1.5% per month or a simple fixed annual percentage rate (APR) of 18% on the financed amount) and flexible repayment terms of 3-6 months, extendable up to 12 based on need and eligibility. Pay only for what you use, with no penalties for early repayment, giving you complete control over your funds and how you manage your business cash flow.

- Efficient and frictionless process: The paperless application process takes only 10 minutes, and you get funding approval in as little as 24 hours. With minimal documentation required, you can easily connect your store across platforms and access the capital you need.

How to Apply for a Line of Credit for your Purchase Orders with CrediLinq

Applying for a line of credit with CrediLinq is a straightforward and digital process designed to provide your business with the funds it needs quickly. Here is how you can go ahead:

Step 1: Start the application

Start your application process by entering email address and phone number

Visit the CrediLinq portal and start by entering your email address and phone number in the brief application form. You can also choose to sign in with your Google and Microsoft account.

Step 2: Enter your OTP

Verify your email with a 4-digit OTP to continue your application

Enter the 4-digit OTP sent to your email to verify your identity and proceed with the application.

Step 3: Provide personal and company details

Provide basic details about yourself and your business to continue

The next step is to fill in your business and personal details, including your name, company name, email address, phone number, date of incorporation, country of registration, and company type, to proceed with the application. You will also add how much funding you want to raise.

Step 4: Connect to e-commerce marketplaces

Securely link your marketplaces to assess your funding eligibility

Once you’ve entered your personal and business details, the next step is to link your e-commerce marketplaces. CrediLinq allows you to connect major marketplaces like Amazon, eBay, TikTok Shop, Shopify, Lazada, Shopee, and more to assess your store performance and funding eligibility.

After submitting your information, CrediLinq conducts an eligibility check. While approval can be obtained within 1 business day, actual disbursement of funds typically takes as little as 3 business days. Upon approval, you can select your desired funding amount, tenure, and the purpose of the funds.

Do Not Let a Big Order Go Unfulfilled

Large orders are a great opportunity to grow your business, but they can be difficult to fulfill without sufficient cash flow or the right financing. PO financing is a common solution, but its limitations, such as rigid fund usage and coverage gaps, can leave you looking for alternative sources of capital.

CrediLinq offers a more flexible solution with its revolving line of credit. With no hidden fees, the ability to use funds across various business needs (marketing, inventory, payroll), and coverage for potentially up to 100% of your purchase orders, CrediLinq empowers you to scale without restrictions.

The platform supports merchants in the United States, the United Kingdom, and Singapore. Unlike competitors like Wayflyer and Parafin, which are focused predominantly on Western-centric platforms, CrediLinq caters to a global market, including e-commerce giants across both East and West, such as Amazon, Shopify, eBay, Lazada, Shopee, TikTok Shop, and more.

Explore your eligibility on CrediLinq today for funding options tailored to your business.

Start with CrediLinq Today!

FAQs

1. Can I use a line of credit to fund purchase orders?

Yes, a line of credit is an excellent option to fund purchase orders. It provides you with flexible, on-demand access to capital that you can use to pay your suppliers upfront, ensuring timely fulfillment of large orders.

2. What is the difference between a line of credit and PO financing?

PO financing is a specific loan that pays your supplier directly to fulfill a particular order, whereas a line of credit is a revolving credit facility. This means you can access funds repeatedly for various business needs, including purchase order funding, giving you greater flexibility and control over your capital.

3. Which is better for small businesses—a line of credit or PO financing?

The right choice depends on your business needs:

- Line of credit: Ideal for businesses that need flexible, reusable capital to cover multiple purchase orders and ongoing expenses like expansion, marketing, inventory, or payroll.

- PO financing: Best for businesses that need funding tied to a specific order or have irregular purchase patterns, especially if they prefer order-specific financing.

4. Is a line of credit cheaper than PO financing?

Generally, a line of credit is more affordable. Lines of credit often have lower interest rates and fewer fees compared to PO financing, which can come with higher processing fees, administrative charges, and advance rates.

5. Do I need collateral for a line of credit or PO financing?

PO financing generally does not require traditional collateral but is secured against the purchase order and the future payment from the customer. A secured line of credit may require collateral, such as inventory or receivables. CrediLinq typically uses your e-commerce store data to assess eligibility, providing a more straightforward path that does not require traditional assets.

6. Can I use both a line of credit and PO financing together?

Yes, many businesses use a combination of both. A line of credit can cover ongoing working capital needs, while PO financing can be used for one-off large orders that exceed the available credit line. Using both strategies diversifies your funding sources and provides greater financial flexibility.

7. What are the risks of using a line of credit for PO funding?

The main risk is overextending your credit if not managed carefully. Interest and fees can accumulate, so it is crucial to manage your repayments promptly to avoid damaging your cash flow or increasing unnecessary costs. However, since you only pay for what you use with a line of credit, you can better control your borrowing and reduce the risk of overextension.

8. When should I choose PO financing over a line of credit?

You might opt for PO financing when you need financing for one-off or infrequent large orders rather than continuous working capital needs. It’s also a good option if your business lacks strong credit history or collateral, since PO financing primarily depends on the buyer’s creditworthiness instead of your own.