TL;DR

- Amazon Lending is either invite-only or relies on a panel of third-party lenders to provide funding to e-commerce sellers. The available offerings are limited to term loans and merchant cash advances, which may not fit every seller’s needs.

- Alternative lenders like AccrueMe, Uncapped, Payoneer, Onramp, and Fundbox offer varied models (profit-share, term loans, receivables advances, and credit lines), each with unique pros and trade-offs.

- CrediLinq, an approved Amazon lending partner in 16 markets, offers a credit line up to USD 2M based on your store’s sales performance.

Why this matters to you

- Cash runs out faster than Amazon payouts arrive, and you need a way to secure a consistent cash flow. A steady stream of funding is what lets you restock on time, keep ads running, and scale your operations.

- It is more than just loans; you need a buffer that gives you room to grow, not just survive.

The Background

Amazon supports small sellers, but when it comes to lending, eligibility depends on meeting their specific criteria.

Platform giants tend to prioritize risk profiles first. That means capital tends to flow toward sellers with long track records, predictable volume, and proven stability.

Smaller retailers who have to work with thin margins and limited working capital rarely tick these boxes.

On Amazon, though, small and medium-sized businesses are central to the marketplace, driving over 60% of sales. In 2024 alone, more than 55,000 independent sellers crossed USD 1M in revenue.

To keep that engine running, Amazon offers financing for sellers through

- Term Loans

- Business Lines of Credit (BLoCs)

- Merchant Cash Advances (MCA)

It makes sense that Amazon is the first port of call for most lenders, and for two practical reasons—signal and speed. Amazon invites sellers based on performance data from sales history, account health, and returns, so the offer, if you get one, would align with your store’s operating reality.

Amazon shows these offers inside Seller Central, which minimizes documentation and context switching.

Most decisions arrive in 1-2 business days, making it attractive if you are timing wholesale inventory turns or Prime Day pushes.

The loans available include:

- Amazon Lending (Invite-Only): You cannot apply yourself; Amazon pre-selects or pre-qualifies sellers to see lending offers. The lending tab appears only for those who meet their internal eligibility metrics.

- Amazon Lending Partners (Apply-Direct): You can apply directly through Seller Central’s Appstore (e.g., CrediLinq, YouLend, SellersFi).

- Outside Lenders – Entirely separate from Amazon (e.g., Wayflyer, Clearco, traditional banks).

So why aren’t all sellers tapping into Amazon Lending?

Since Amazon uses internal metrics to decide who qualifies, it may be difficult to become eligible for funding. Most new or fast-growing sellers never see an offer.

If Amazon holds back the credit tap, smaller sellers are left searching for financing models that actually match the tempo of digital retail.

We have conducted research to provide you with Amazon small business lending options so that you can keep pace with inventory cycles and ad spend.

Amazon’s Lending Options at a Glance

Here’s how Amazon’s lending offers compare:

Top Alternative Amazon Lending Partners

1. CrediLinq (best for multi-platform sellers who want flexible, no-equity capital)

CrediLinq is an approved Amazon lending partner in 16 markets. Instead of traditional loans, the platform offers a line of credit for online sellers. It connects directly to your Amazon store data to determine your credit line limit, offering up to USD 2M.

It supports and links directly to your stores on multiple platforms beyond Amazon, including TikTok Shop, Shopify, eBay, Lazada, Shopee, and more so underwriting reads your actual sales performance on each one. You can connect or upload data wherever needed.

You pay a flat monthly service fee as low as 1.5% per month [or a simple, fixed annual percentage rate (APR) of 18% on the amount you actually use, with no hidden charges. And unlike revenue-share models, CrediLinq never takes a cut of your sales, profits, or equity.

|

Suggested read: Difference Between Revenue vs Equity Financing |

You can draw as per your needs and choose 3-6-month repayment periods (biweekly installments). The credit line solution acts as a standby source of funds, for which you are only charged for the amount you utilize. There is no lock-in period and you can pay back early at any time with no penalties.

|

CrediLinq eligibility and coverage for Amazon business loans: You’re eligible for CrediLinq’s line of credit if you:

CrediLinq’s simple application process allows you to avoid mundane paperwork.

*Basic KYC still applies (business registration, tax ID, shareholder/director ID and address). Additional documents may be requested in some cases.

CrediLinq geo-availability: Loans from the platform are currently available in three regions:

CrediLinq is also cross-border friendly with disbursements in USD, GBP, and SGD, depending on the seller’s preference.

CrediLinq’s approval speed: In principle approvals can be offered as fast as 1 business day.

CrediLinq’s repayment model: Flat fees as low as 1.5% per month or a simple fixed annual percentage rate (APR) of 18% on the amount you draw, with flexible repayment options of 3-6 months in biweekly installments. *Customized solutions are available upon request. Loan tenors can extend up to 12 months on a case-by-case basis. |

Pros of CrediLinq for Amazon business owners

- Easy to access credit line: Simply connect your store, get approved quickly, and draw funds as needed.

- Transparent pricing: Single fee, no hidden add-ons or FX markups.

- Multi-purpose funding: Use capital freely for cross-border growth, marketplace expansion, product launches, inventory restock, and ads.

- Flexible repayment: Choose 3-6*-month repayment plans with no penalties for early repayment.

- No equity dilution: Keep full ownership of your business – CrediLinq provides working capital without taking any shares.

Things to note so you’re not surprised

- CrediLinq prioritizes shorter tenures by design (3-6 months), which is great for fast cycles but less ideal if you want a 2–5 year amortizing loan.

- A business entity is required, so individuals or sole proprietors are not eligible

2. ClearCo (best for non-dilutive working capital)

Ecommerce funding solution by ClearCo for Amazon Businesses (Source: ClearCo)

ClearCo offers revenue-based financing to ecommerce brands by connecting to your Amazon, Shopify, PayPal, or Stripe accounts. You can choose between invoice funding, where ClearCo pays vendors directly, or a cash advance deposited into your account.

To be eligible, you need at least 12 months of business revenue over USD 10K per month, along with incorporation (LLC or corporation), and access to a U.S. bank account.

|

ClearCo geo-availability: Funding provided for eCommerce businesses in the United States, United Kingdom, Ireland, Netherlands, Australia, and Germany. But businesses must have a United States checking bank account.

ClearCo approval speed: For invoice processing, the application is reviewed in 1-2 business days, and deposits are often completed in 0-3 business days. Brands can fund up to USD 1 million in receipts over 60 days (max USD 500,000 per draw).

ClearCo repayment model: You repay via fixed, capped weekly remittances based on your sales, plus a flat fee between 3.63% and 12.5% depending on your extension plan. |

Pros of ClearCo loans for Amazon business owners

- Fast, data-driven funding decisions in 1-2 business days

- Predictable weekly payments and no collateral or personal guarantees

Cons of ClearCo loans for Amazon business owners

- Requires a U.S. legal and banking setup, less accessible for non-U.S. sellers

3. Uncapped (best for established brands needing large growth loans)

Capital loan funding by Uncapped (Source: Uncapped)

Uncapped offers term loans and working-capital lines of credit to high-revenue sellers with at least USD 100K+ in monthly sales.

Funding limit ranges from USD 100K – USD 10M, depending on the product type and business performance.

Offers include:

- Amazon Seller Financing (daily payout deductions)

- Growth Working Capital (fixed fee over term)

- Line of Credit for sellers with USD 5M+ annual revenue

|

Uncapped geo-availability:

Uncapped approval speed: Draws available in 1-2 business days for a line of credit with immediate funding after approval.

Uncapped repayment model: Fixed fee (0.70% – 1.5% monthly base). For a two-month term, the base fee is 2% and for a six-month term, 6%. |

Pros of Uncapped loans for Amazon business owners

- Transparent flat fees, often lower than MCA or equity-based alternatives

- Flexible repayment options (options to pay back in daily, weekly, and monthly installments)

- Startup-friendly with low tenure requirement (accessible after just six months in business)

Cons of Uncapped loans for Amazon business owners

- Requires high and consistent revenue, which may exclude lean sellers

4. Payoneer Capital Advance (best for cross-border sellers)

Capital Advance loans by Payoneer (Source: Payoneer)

Payoneer gives working capital advance tied to your marketplace receivables. It is available for Amazon.com, Amazon.co.uk, and Walmart sellers. Limit ranges as far up to 140% of your monthly volume, and is capped at USD 750K.

Payoneer offers a fixed fee that’s auto-deductible from future Amazon payouts.

To be eligible, you must have at least 6 months of selling history on Amazon and maintain steady receivables volume through Payoneer.

|

Payoneer geo-availability:

Payoneer approval speed: Funds are sent minutes after accepting an offer.

Payoneer repayment model: Auto collection as a fixed percent of incoming marketplace payments until the loan is settled. |

Pros of Payoneer loans for Amazon business owners

- Rolling offers after good standing

- No interests, just a flat fee from the start

Cons of Payoneer loans for Amazon business owners

- Only available to sellers already using Payoneer for Amazon payouts

5. Onramp funds (best for fast-moving Amazon shops with seasonal spikes)

Funding by Onramp for eCommerce brands (Source: Onramp)

Onramp provides sales-based financing for eCommerce (including Amazon, Shopify, TikTok Shop, WooCommerce, BigCommerce, Squarespace, Walmart, and Shopline). You can get funding for up to USD 2M with a fixed fee of 2% – 8%.

All you need is at least a record of USD 3K in average monthly sales with no minimum months in business required.

Furthermore, consideration is a data-driven underwriting that uses your Amazon sales data with a focus on consistent average revenue.

|

Onramp geo-availability: Targets only U.S. e-commerce brands.

Onramp approval speed: Often same or next business day decisions.

Onramp repayment Model: Flexible repayment based on a percentage of daily Amazon sales. Fees are pegged from 0.5% – 4% of your sales (estimated APR equivalent of 11.9% – 19.9%, depending on the terms of your advance. |

Pros of Onramp loans for Amazon business owners

- Cash-flow alignment via percentage-of-sales repayment

- Approval focuses on revenue performance, not credit scores

Cons of Onramp loans for Amazon business owners

- Requires steady sales to qualify

- Effective fees can be high depending on the repayment timeline

Quick Comparison: Amazon Small Business Lending Partners

*Customized repayment plans available. Loan tenors can be extended to 12 months on a case-by-case basis.

Why Choice Matters for Amazon Sellers

If you stop receiving sales or payments today, your small business can keep paying expenses for just 27 days before running out of money.

For fifty percent of small businesses, the cushion is thirty days or less. After that, they wouldn’t be able to cover ongoing costs without new income or external funding.

You need to have other financing options for your e-commerce business and can not rely on only Amazon’s source of credit. Why?

- Invite-only is a hurdle – If credit only shows up when you’re “eligible,” what happens when the offer arrives after your supplier window closes? Or never arrives at all?

- Speed decides outcomes – Digital retail moves in hours. Suppliers want deposits now. Ads hit their pace now. If funding takes days longer than your sales cycle, you may have to deal with stock-outs, higher freight, or worse, lost rank.

- Cash-flow alignment – Fixed, calendar-based payments don’t always match how Amazon pays you. Sales spike and then slow down all the time. The financing you choose should be in sync with that flow. You should be able to:

- Pay more when you sell more and less when you don’t

- Draw only what you need and when you need it.

- Transparency – You need to know, upfront: how much lands in your account, what gets deducted, and the real total cost over your payback window. “Simple, single fee” is more valuable than a low headline rate with layers underneath.

How to Choose the Right eCommerce Funding Partner

The number ceiling is important, but that’s not all that matters. The terms and conditions are very crucial in picking the right loan partner. Look out for:

1. Business eligibility

The minimums that are consistent with many funding partners are months selling, annual/monthly revenue, and a registered entity versus sole proprietorship. Look for partners that have criteria where you exceed the minimum. Also, ensure the partner can increase your limit by 3–5x as your throughput scales.

2. Application approval simplicity

You may want to avoid platforms that have a lot of friction profiles. Look out for partners that require lighter documentation (basic KYC) as against tax returns and bank statements. CrediLinq leans on just your preferred platform and Plaid/bank account data; Onramp integrates with marketplaces for information; it should be as easy as that.

Take note of the time from acceptance till funds in your account, and how long an offer stays valid before it expires. Rolling facilities (credit lines) avoid repeated applications but embedded programs sometimes require fresh applications each time and might lead to unnecessary delays.

3. Transparent fees and total cost

Make sure your selected funding partner clearly states their fee model. Some installment or line facilities charge a flat monthly service fee only on what you draw and usually have no early-pay penalties. This is good as it makes things predictable and easy to budget. CrediLinq, for example, provides this type of solution.

Sales-based products take a fixed fee and collect a percentage of sales; they flex with revenue but things can get pricey if repayment drags (e.g., Onramp, Clearco, Payoneer).

Fixed-fee offers with a minimum term sit in the middle. It is “semi-predictable,” but you must check the true cost if you repay early (like with Uncapped).

4. Credit limit range

The number matters, but what matters more is whether it grows with you. A US$ 50,000 line might be fine when you’re running two SKUs, but may not serve well once you scale into five marketplaces.

Look for:

- Scalability: How quickly and how often does the lender refresh your limit? Monthly reviews tied to sales performance are better than annual resets.

- Growth path: What is the documented runway (e.g., CrediLinq scales up to US$ 2 million; Payoneer caps at US$ 750,000)?

- Utilization rules: Does using 70–80% of your limit trigger an automatic bump, or are you stuck reapplying?

5. Flexibility of fund usage

Where can the money actually go? Now some programs like Uncapped credit a marketplace wallet and get repayments from payouts which is great for speed but quite limiting for non-marketplace spend.

By contrast, credit lines that pay into your bank account give you freedom. You can use funds for inventory, logistics, ad campaigns, freight costs, packaging, or tooling (wherever your working capital is stretched).

Also, the degree of cross-border flexibility is important.

Can you wire money to overseas suppliers in their local currency without absorbing heavy forex spends? Does the provider let you pay 3PLs, ad networks, or freight forwarders directly?

These details decide whether capital actually supports your growth or just plugs a narrow gap.

|

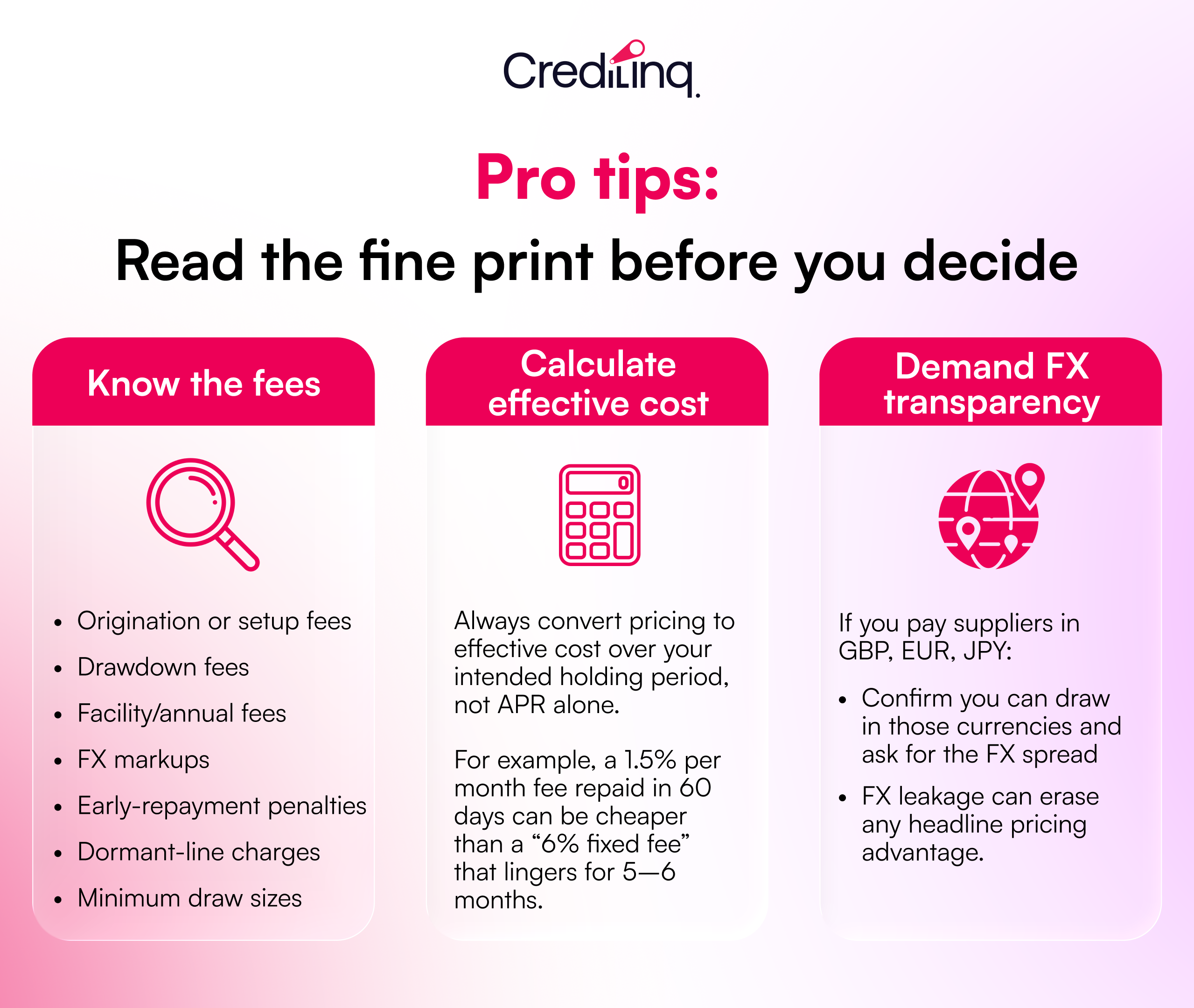

💡Pro tip: Make sure you always match the disbursement currency to your supplier invoices. Otherwise, you risk paying double conversions and leaking margin through FX spreads. |

6. Flexible repayment models

When payouts are not predictable in the long-term, fixed bank-style installments can stifle cash flow. Revenue-based models solve this by scaling with sales, but they take more in your busiest months.

Onramp Funds is a good example: they deduct a small percentage of daily Amazon sales, so you pay more when sales are high and less when they dip.

CrediLinq balances the two, repayments are fixed but only across 2–4 months, so you know exactly what goes out and are not locked into years of stretched installment repayments.

This gives you enough room without losing a sizable portion of every payout.

7. Minimal documentation and fast decisions

Waiting weeks for approvals while compiling tax returns puts another hurdle in your way for an otherwise fast-moving industry.

CrediLinq leans on the platform data and connects to your Plaid account. By connecting your Amazon store, it underwrites your sales performance. So you don’t have to file tax returns or other paperwork, just basic KYC. Approvals are often in as little as one business day.

8. Credibility and scale

You want a funder who won’t disappear when your needs grow.

CrediLinq is an approved Amazon lending partner in 16 markets. That official status signals stability and integration, and the revolving credit line scales from $50K up to $2M, giving you plenty of headroom as your store grows.

Capital Funding as Control

In the end, funding isn’t about debt but control. Control over when to restock, how fast to expand, and whether you act on opportunities or watch them pass.

Choosing the right partner now means you’re ready when the next window opens.

Get funded today with CrediLinq and see how quickly that control can shift back into your hands.

Frequently Asked Questions (FAQs)

Does Amazon do small business loans?

Yes. Amazon Lending offers term loans, lines of credit, and merchant cash advances, but only on an invite-only basis using internal seller performance metrics.

Does Amazon give small business grants?

Yes, through its Amazon Business Small Business Grants, Amazon awards over USD 250,000 in grants and prizes to 15 U.S.-based small businesses annually, including cash awards up to USD 25,000, plus perks like Business Prime and device bundles.

How fast can Amazon sellers access funds through alternative lenders like CrediLinq?

CrediLinq approves within one business day by connecting directly to your store data and disburses funds shortly thereafter, much faster than most traditional banks.

Why choose CrediLinq over Amazon Lending?

CrediLinq offers a revolving credit line with transparent pricing and short, fixed terms. Repayment is flexible over 3-6 months with no hidden charges. Unlike Amazon Lending, it is not invite-only and does not auto-deduct fees directly from payouts.