TL;DR

- Inventory financing isn’t just for big brands with large warehouses and years of history—newer options consider your actual sales and cash flow.

- Traditional financing can be costly and complicated, with unclear fees, lengthy paperwork, and the risk of losing inventory.

- Modern solutions offer flexible terms based on sales data, purchase orders, and business health, making working capital accessible to growing ecommerce sellers.

- Choosing the right option means understanding eligibility, fee structures, and repayment terms to get capital on your terms without unnecessary risk.

Many sellers assume they need massive inventory, years of experience, or hard collateral just to qualify for inventory financing. That it’s only reserved for big brands with warehouses full of stock and deep financial history.

And when you’re already tight on cash, the idea of taking on debt feels risky. Add to that the confusion of unclear fees, lengthy paperwork, and the fear of losing your inventory if something goes wrong, and it’s no surprise that most sellers hesitate.

But not all financing works that way.

Today, newer financing options take a different approach. Instead of focusing solely on how much inventory you’re holding, they look at the actual health of your business—your marketplace sales, purchase orders, and day-to-day cash flow.

This shift means even growing brands can now access working capital on flexible terms without putting everything at risk.

In this blog, we’ll break down the technical side of the inventory financing option, covering eligibility, fees, and repayment structure, so you can confidently choose what works best for your business.

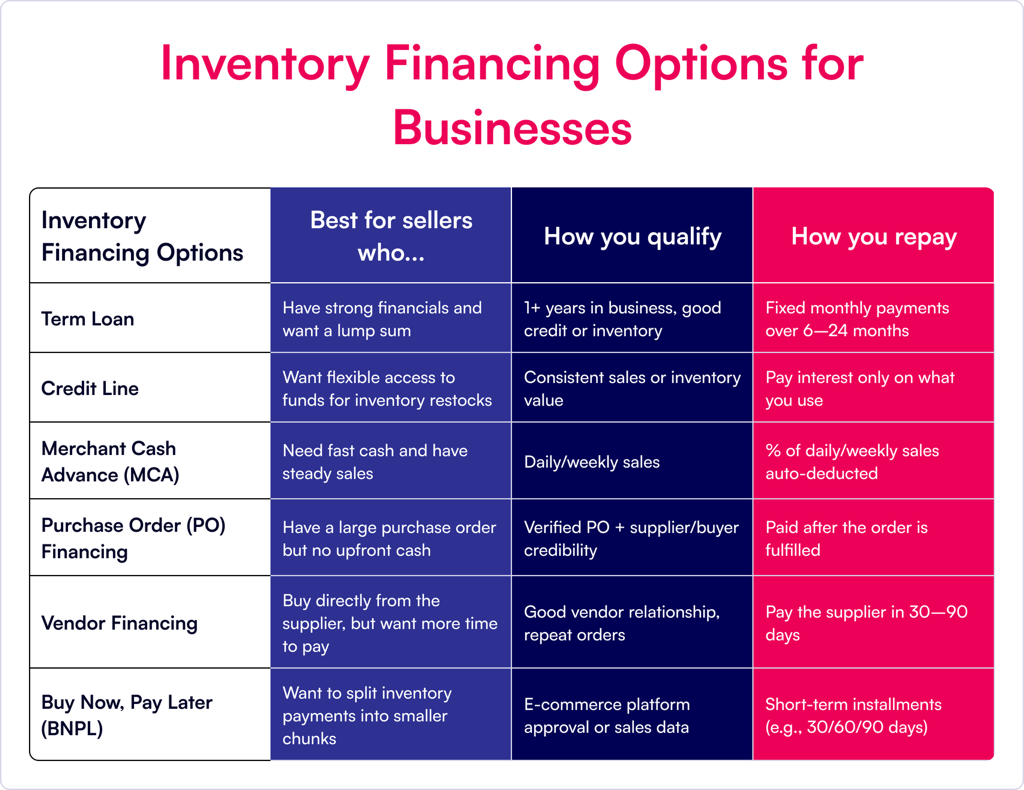

An Overview of Inventory Financing Options for Businesses

If you’re exploring inventory financing, you’re likely asking two key questions:

- What will it actually cost?

- Will my business qualify, without putting existing inventory or cash flow at risk?

To help you answer that, here’s a quick overview of the most common inventory financing options, along with how they work, so you can identify what best fits your current needs.

Understanding Inventory Financing Fee Structures: APR vs Fixed Fee vs Factor Rate

Inventory financing lenders use very different ways to present costs. They don’t always say “interest rate” like a normal loan.

Instead, they say:

- “1.5% monthly interest” — meaning every month you pay 1.5% of the loan as interest.

- “$1,000 flat fee” — a fixed amount you pay no matter how long you take.

- “1.2x factor rate” — meaning if you borrow $10,000, you pay back $12,000 total.

These all look very different, so how do you know which is actually cheaper?

This is where the annual percentage rate (APR) helps. It shows the true yearly cost of borrowing, including fees and interest, as a percentage.

*An example to explain the difference, doesn’t represent specific product’s fees*

*Note: Assuming $10,000 is borrowed twice for 6 months each

Interest-based products look cheaper upfront, but if repayment drags on or revenue slows, the cost climbs. In contrast, fixed fees are upfront and simple, but don’t reward you for repaying early.

Average Inventory Funding Interest Rates

Now that you understand how to interpret financing costs, it’s helpful to see how those play out in practice.

Below, we’ve listed the average APR ranges for common inventory financing options, so you can get a clearer sense of what to expect and how each one stacks up against the others.

| Financing Product | Typical Fee Structure | Average Inventory Financing Rates | When It’s a Good Fit |

| Loans | Interest rate (APR, often fixed or variable) | 6%–36% APR for online lenders (Traditional banks offer lower rates but stricter requirements.) | When you need a lump sum for a large inventory purchase, have predictable cash flow, and can meet documentation/credit requirements |

| Credit Line | Interest rate (APR, only charged on the drawn amount) | 6%–86% APR for fintechs (typically 10%–30% for established borrowers) | For expansion, flexible inventory needs, covering cash flow gaps, or taking advantage of supplier discounts |

| MCA | Factor rate (e.g., 1.1–1.5x advance), fixed fee repaid via % of daily sales | Factor rates equivalent to 20%–50%+ APR (Effective APR can be higher due to daily/weekly repayments) | When you need very fast funding, have strong sales but weak credit, and can handle frequent repayments |

| PO Financing | Factor rate or interest + fees (based on purchase order value) | 1.5%–6% per month (effective APR 18%–72%) | For businesses with large purchase orders from reputable buyers but insufficient cash to fulfill them |

| Vendor Financing | Fixed fee or interest (sometimes 0% for promotional terms) | 0%–24% APR (often interest-free for short terms (30–90 days)) | Good for cash flow management and supplier relationship building |

| BNPL | Fixed fee or interest (often 0% for short term, then interest applies) | 0%–30% APR (typically 0% for 30–90 days, then 1%–3% per month if unpaid) | Useful for startups or businesses with limited credit history seeking short-term flexibility |

How to Pick the Best Inventory Financing for Your Business

Inventory financing can feel complex, but breaking it down into three key factors—eligibility, fees, and repayment structure—helps you make a clear choice.

- Eligibility: Different lenders have varying requirements — some need your business to be at least 1–2 years old, others focus more on your sales data or inventory value. Understanding what you qualify for helps you narrow down your options.

- Fees: Inventory financing can come with interest rates, fixed fees, or factor rates. Each affects your total cost differently, so it’s important to compare these fee structures carefully to avoid surprises.

- Repayment Terms: Repayment schedules range from flexible credit lines to daily or weekly payments tied to sales. Choose terms that align with your cash flow to keep your finances manageable.

This targeted approach makes inventory financing accessible and practical—even if you don’t have massive stock or years of history.

Inventory Financing, Simplified for Every Seller

Inventory financing is no longer limited to businesses with large stockpiles or long-established financial histories. Thanks to new funding options, even new and growing sellers can access capital on flexible, transparent terms.

These modern solutions eliminate the traditional hurdles—no more needing massive inventory, extensive paperwork, or hard collateral to qualify. Instead, you simply connect your online stores, and funding decisions are made based on your actual sales data and business performance.

With these options, you maintain control and avoid the risks and complications. Ultimately, getting the funds is now simpler and more accessible than ever, giving you the freedom to grow your brand on your own terms.